JOLTS Recap (April)

Holding steady, but choppier waters in May?

TL;DR: The pause in labor market cooling as measured by turnover data continued through April, despite the April 2nd tariff announcement. But data from May suggest the possibility of renewed cooling ahead.

Besides this JOLTS recap, I’ll be publishing a lot this week:

The BLS jobs report preview on Wednesday (which will include a recap of the Q4 QCEW data)

The usual high frequency labor market indicator recap on Thursday

The BLS jobs report recap on Friday

The remainder of this piece covers:

The Big Picture

Data Roundup

More below chart.

1. The Big Picture

Turnover data from the JOLTS report is among our best barometers of labor market warmth, and what we’ve seen since last summer is a clear stabilization in the labor market.1 Hiring stopped falling first; quits followed a few months later. And while layoffs have gone up a little, there’s no sign of an ongoing acceleration - just a small, one-time persistent increase.

It’s noteworthy that today’s data corresponds to April. Hires, layoffs and quits cover the entire month; openings come from the last business day. That’s a lot of time post-dating the shocking April 2nd tariff announcement. But we already know from a bunch of other data sources that very few businesses reacted immediately, especially on the headcount front.2

There’s some evidence patience began to run out in May from our timeliest data source, claims for unemployment insurance. These have accelerated a little recently, which indicates some combination of falling hiring and rising layoffs. If I was a betting man, I’d expect the hiring side of the ledger to move more than the layoff side - so we may be due for slightly weaker JOLTS data next month. I don’t have a strong opinion on whether this is a small one-time deterioration or the first step in a larger descent.

2. Data Roundup

The hiring rate rose to 3.5% in April. That’s the highest since September of last year, though it’s still pretty weak: it matches the level in the spring of 2014, when the unemployment rate was 6.4%. It’s still hard to find a job!

The quit rate came back down to 2.0% - comparable to where it was from the summer of 2015 through early 2016, with an unemployment rate slightly above 5%. People know there aren’t many opportunities out there, and are staying put.

Layoffs remain very low by historical standards - lower than you would expect given the current unemployment rate (4.2%). They are higher than they were a year ago, but this appears to have been a one-time increase.

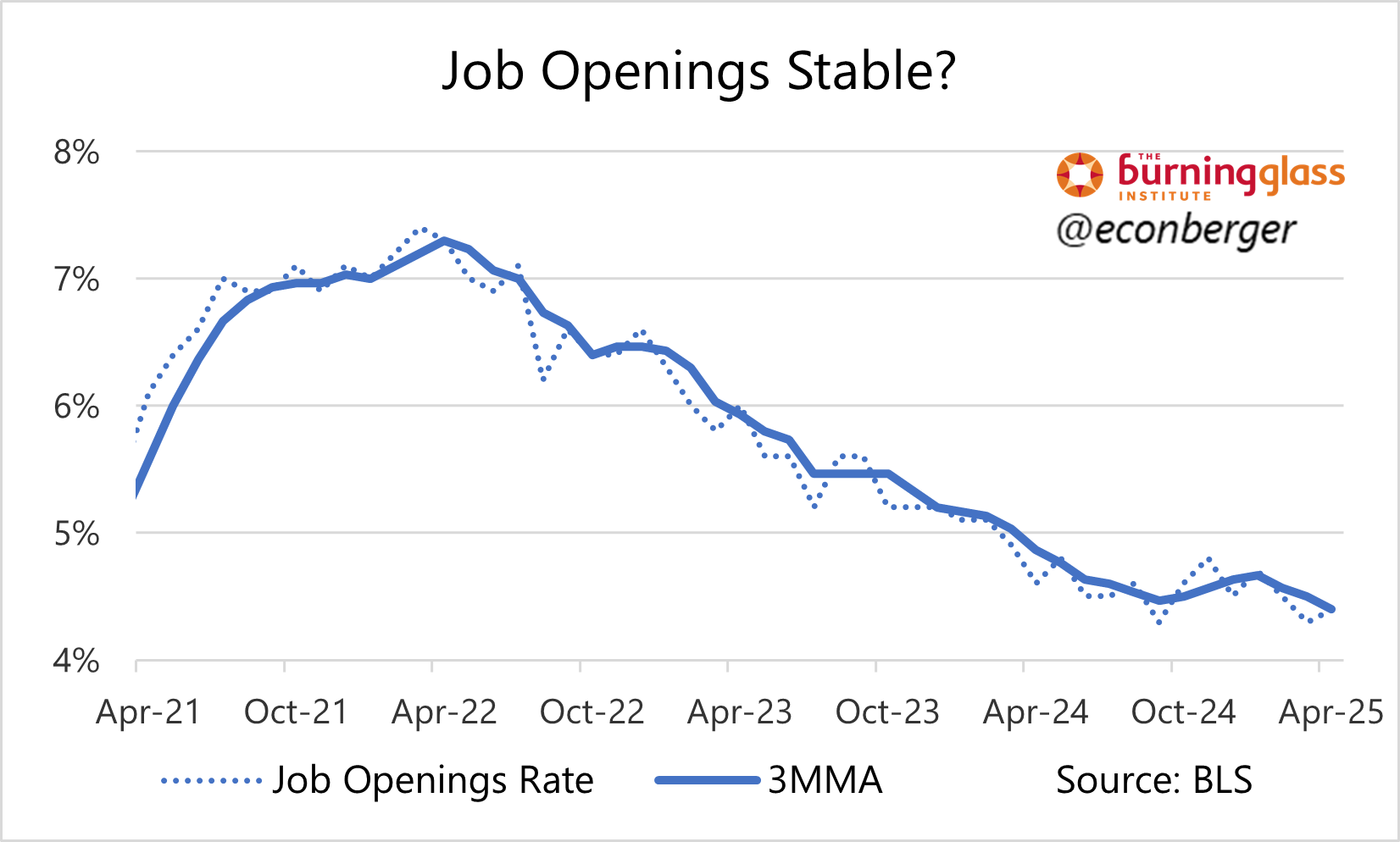

Long-time readers know I prefer the turnover data to the openings data, but one advantage of the latter in a fast-changing environment is its timeliness; it covers the end of the month instead of its entirety. But openings are also showing a moderation and possibly pause in the cooling process through April:

To wrap up, if there wasn’t a lot of other stuff going on, I’d feel pretty good (not great) about this data. It’s a tough time to find a job, but at least it’s not getting worse! But the recent resilience is going to be tested.

This stabilization through April is also apparent in the monthly jobs report.

This patience was vindicated when a lot of the tariffs were paused (indefinitely?).