BLS Jobs Report Preview (February)

Cold hiring weather ahead, but not this month

TL;DR: Policy decisions being implemented will weaken the labor market going forward, but only a little of that damage is likely to land in the February jobs report.

This piece includes 2 sections:

The Big Picture: Renewed Cooling

This Month’s Report

More below chart.

1. The Big Picture: Renewed Cooling

A few months back, when I wrote my 2025 labor market preview, in order to dot my i’s and cross my t’s, I included a downside risks section and flippantly wrote the following:

A combination of higher tariffs, sharp cutbacks in government spending without large cuts in other taxes or easing in monetary policy leads to lower aggregate demand and weaker labor markets. This seems like a fanciful scenario!

Fanciful or not, here we are! We still seem pretty far from the anticipated tax cuts; tariffs have gone up (but may come down again?) and we’re seeing large scale layoffs of the federal government workforce (though also no sign that government spending growth has slowed). Measures of economic policy uncertainty are skyrocketing. And at least some administration-affiliated politicians are expressing a “no-pain, no-gain attitude”.

All this is starting to wear on US employers. As of 2/23, before the most recent wave of negative policy news, employer plans to expand future headcount (which had an optimistic 3 month run after the election) have already returned back to year ago levels.

As recently as 4 weeks ago, I confidently pronounced that the US job market was stabilizing. But I think we’re going have to dial back that probability substantially, and up the risk of a renewed cooling. With luck, that cooling will be of the gradual non-recessionary nature we experienced during 2022-2024, and other policy levers will eventually come into stabilize the situation. TBD!

2. This Month’s Report: Too Soon for a Big Impact

Now that I’ve expressed my pessimism about the coming year, let me add that I don’t think we’re going to see much of an impact in Friday’s report. Most significantly, the reference period for this report is February 9th through 15th. The big federal government layoffs weren’t announced until the back half of that week; from the perspective of both the household survey and the establishment survey in the report, everybody impacted would still count as employed.12

However, some sources of weakness could come earlier. A freeze of federal hiring was announced on January 20th. There are about 30K federal workers hired every month, so it’s possible that we’ll say net employment gains in the sector contract by 20K-25K. (It’s also possible that quits by disillusioned federal government workers picked up during this period, which would drag the number down further.)

Additionally, various disruptions to government outgoing payments may have already caused some job losses from entities dependent on those payments; here is one example. My guess is this effect was pretty small, as of February. Job losses here would show up outside of the federal government, in state and local governments or private sector industries, and (at least for the time being) would be hard to disentangle from the usual monthly noise in those sectors.

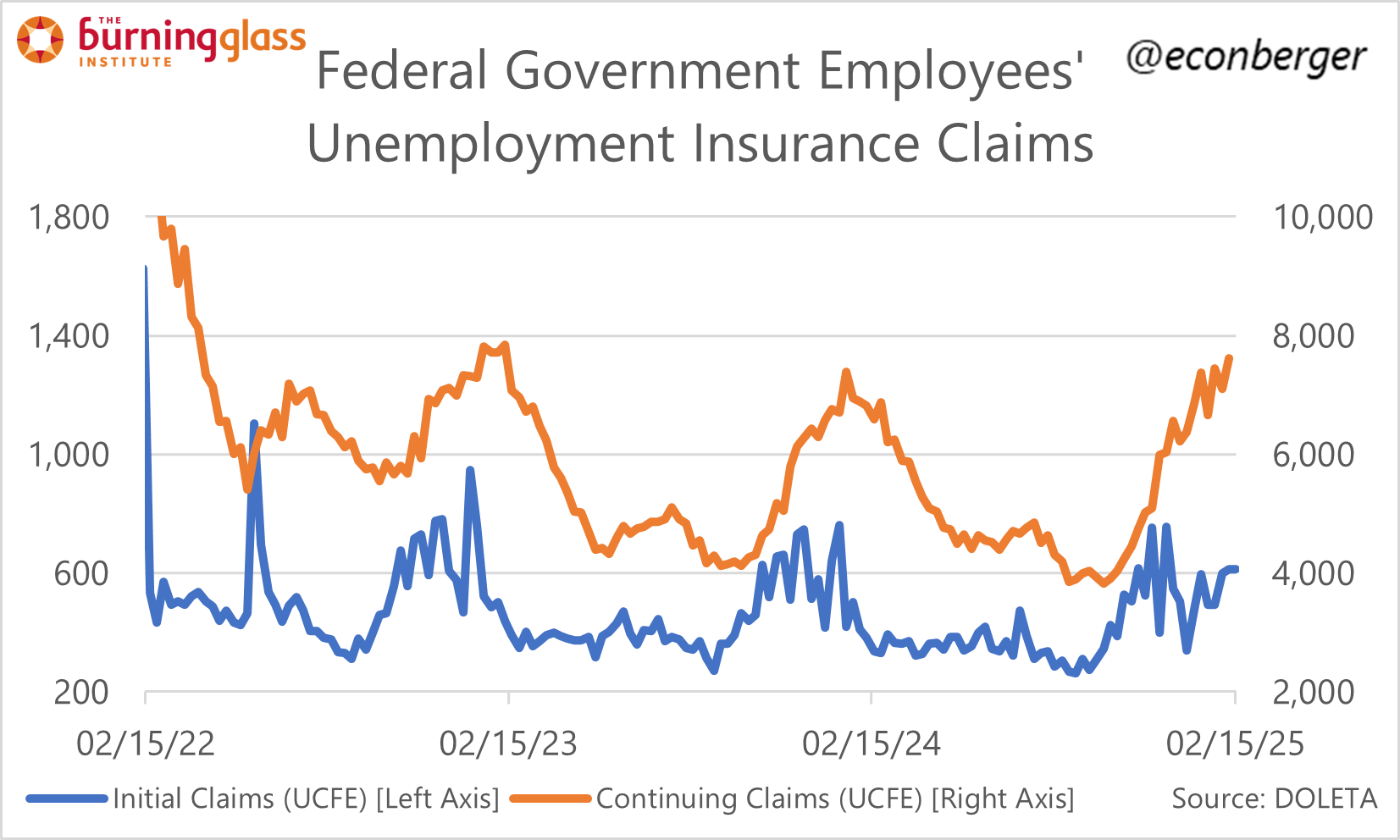

The jobless claims data is one of our best “hard data” sources and at least through the payroll survey period, the impact on layoffs seems to be small. For instance, regular initial claims (which exclude federal workers) had been running only modestly above year-ago levels through February 15th. The spike in the February 22nd data was more substantial but, assuming it’s not noise, is reflective of developments that will show up in the next report, not this one. The other key time series, initial claims series for federal workers (UCFE), remained at very low levels through the survey period; I expect this will change, but that’s also a story for future monthly jobs reports.

Every once in a while, there’s a phase change in the economy which renders obsolete the “fresh” jobs report - there’s good or bad news coming, but not quickly enough to register in the monthly data. February 2025 may end up being such a case. Time to fast forward 4 weeks!

The laid off folks may be on administrative leave for some time, which would push the layoff date out further.

There are also about 75K workers who took a buyout / early retirement. They will continue to collect a paycheck until early fall, and will remain employed for the purposes of this report as well as a bunch of the following ones.