Preview of the 2024 Preliminary Benchmark Estimate

Negative "old news"

TL;DR: On August 21st, we’ll get “old news” about the state of the labor market with a preliminary estimate of revisions to nonfarm payroll employment growth from March 2023 through March 2024. The revisions are likely to shift growth over that period from “strong” to “solid”.

A table of contents on this piece

What is a benchmark revision?

What to expect?

“Old News”

What won’t change?

What might change?

A common misconception

1. What is a benchmark revision?

Every year, in the January jobs report (released in early February), the BLS applies an annual revision to historical Current Employment Statistics (CES, or establishment survey) data within the report. The most scrutinized revisions are those applied to nonfarm payroll employment, though other widely-reported CES data like hours and earnings are also revised.

An important chunk of that annual revision is application of an employment benchmark to CES data corresponding to March of the prior year.1 Because we think of a lot of CES data in terms of delta rather than in terms of level (e.g. employment growth), the benchmark revision alters not only data from March of the prior year, but also for the entire year before that. So for example, the January 2025 report will directly apply a benchmark revision to the level of March 2024 data, and THAT revision will cause revisions to monthly data from April 2023 (the month after the prior benchmark date) and March 2024.

The reason the BLS does this is because the CES’s sample of establishments can drift off course from representing the economy. Establishments are created (which can lead to undercounts of employment), destroyed (which can lead to overcounts of employment), and the benchmarking exercise is a useful way of correcting that drift.

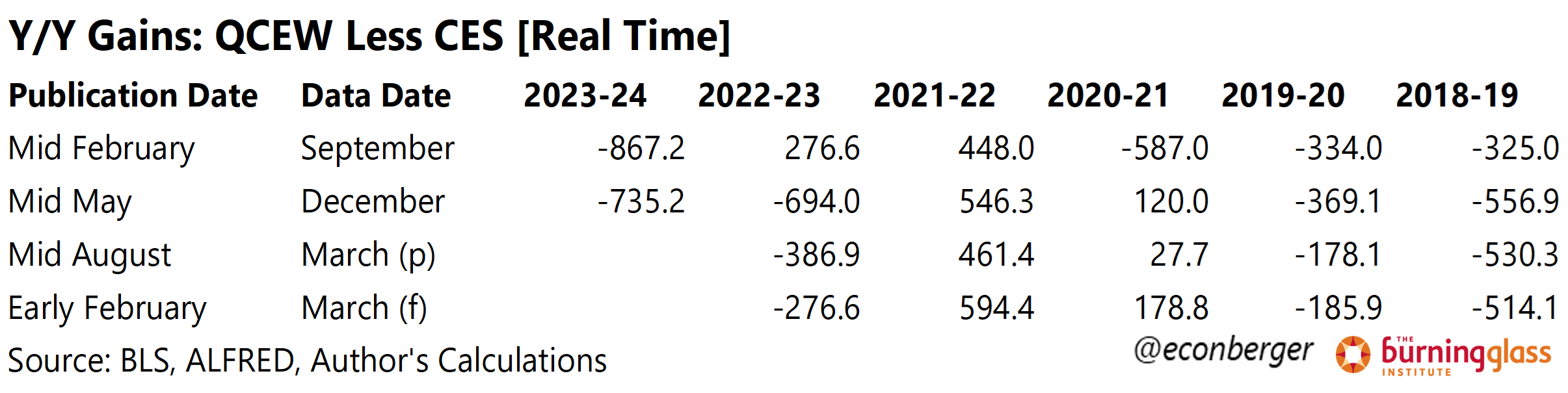

The source data for the benchmark data is the BLS’s Quarterly Census of Employment and Wages (QCEW), which is based on a more thorough universe of data sourced from unemployment insurance data. QCEW data is released with a ~4.5 month lag relative to the CES. For instance, on August 21st the QCEW will release Q1 (January through March) 2024 data; we already have CES data for July. For the CES benchmark, it’s this Q1 mid-summer release that matters the most, because the year-over-year QCEW change as of March generates the CES benchmark revision estimate.

So on Wednesday August 21st at 10 AM ET, the BLS will publish a preliminary benchmark estimate telling us by how much they anticipate the March 2024 payroll employment level to change. They will also include some details of revisions at a major-industry level; these can be interesting, because revisions at the industry level can be quite large even as they offset at the aggregate level.

5.5 months after this preliminary benchmark estimate, there is a final benchmark estimate which is then incorporated into the CES data in early February as described above. The preliminary and final estimates can vary a little because QCEW data is itself susceptible to revisions, but those differences tend to be small. Importantly, we’re going to be staring for quite a while at the unrevised pre-March-2024 data for quite a while even though we realize it is due for a revision.

2. What to expect

We now have 3 quarters of post-March-2023 QCEW data in hand (Q2, Q3, & Q4 2023). On August 21st we’ll get Q1 2024 and that’s what will give us the preliminary benchmark estimate. Those 3 quarters of data indicate that the CES data has been stronger than the QCEW from March 2023 through December 2023 by about 735K; a naive (and probably incorrect) interpretation is that the current CES estimates of month-to-month employment changes during this 9 month period should be revised down by about 82K per month.

The reason this interpretation is probably incorrect is that over the past 5 years, the 3 quarter QCEW estimate has been more pessimistic than the final 4 quarter estimate each and every time - by anywhere from 43K (2018-19) to 417K (2022-23). So not only does it seem unlikely that we’re going to get a downward revision of 82K per month (735K spread across 9 months), but it’s probably too pessimistic to expect a downward revision of 62K per month (735K spread across 12 months). Something like 45K-58K per month is my baseline expectation.

That’s still a fairly hefty revision, but payroll employment gains averaged 242K per month in the year to March 2024. At worst, this means a downward revision from “strong” to “solid”. None of it will look recessionary.

3. “Old News”

Let’s say we get a large implied downward revision to March 2024 nonfarm payroll employment level. I’m a labor market fanatic, not a financial market or Fed guy (much less a “vibes expert”), so for all I know the data we get on the 21st will significantly reorient those entities’ views. I’m mainly interested in the following question: how does our “all in” view of the labor market trajectory change?

My baseline answer: Unless you’re someone who’s been gripping onto very rose tinted goggles, not much. This is stale data from 4.5-16.5 months ago. We have much more recent, non-revisable data from the monthly jobs report (ratios from the household survey) that tells us the labor market is cooling gradually. If you’re looking to update that perspective, the marginal information from this preliminary benchmark is very low.

However… one thing that would give me pause is if 4 quarter CES-QCEW gap widens substantially from the 3-quarter 735K. That would hint (but not confirm) that there’s been additional relatively-recent deterioration in the labor market. The additional information about our current trajectory wouldn’t be very high, but not “very low”.

4. What won’t change

The QCEW and preliminary benchmark leave the Current Population Survey (CPS or household survey), which accounts for much of the key data in the jobs report, untouched. So there will be zero implications for the unemployment rate, the share of the labor force working part-time for economic reasons, labor force participation or the prime-working-age employment-population ratio.

That means the stories household survey data tell us about recent trends in the labor market (which as stated earlier, mostly imply an ongoing gradual cooling) are going to be equally true on August 20th and August 22nd.2

Another important source of labor market data that will be unaffected: the unemployment insurance data. I know the initial and continuing claims data have been a little messy but they’re still indispensable.

5. What might change

Most of the attention from the preliminary benchmark announcement centers around employment (headcount) gains. But there are also implications for other parts of the CES - hours and earnings in particular. For instance, if low paying industries bear the brunt of the downward revisions, that would boost wage growth; if high paying industries bear the brunt of the downward revisions, that would lower wage growth.

Also, we usually don’t talk about it in the context of benchmark revisions, but eventually they’re applied to the JOLTS data. So for example, I’d expect that lower net employment growth will translate into some combination of lower hires, higher quits, and/or higher layoffs.

6. A common misconception

I’ll wrap up this piece with a pet peeves regarding usage of the QCEW data. From the perspective of CES revisions, the intra-year numbers don’t matter. The only thing that matters is the March to March change. So for example - the Q3 2023 QCEW data looked particularly weak. That weakness won’t show up in the CES benchmark revision as particular weakness in Q3 nonfarm payroll growth.

It can be debated whether the excess high-frequently volatility of the QCEW relative to the CES is a feature or a bug. Maybe the quarterly noise in the QCEW is telling us something important about labor market wiggles that the CES ignores. But you cannot infer anything about post-revision CES intra-year wiggles from the QCEW.

The annual revision also includes two other important elements - a revision to seasonal adjustment factors going back several years (which alters the intra-year wiggles but not the overall trajectory), and a revision to more recent data (post-benchmark date) based on the updated net birth-death model.

There are separate issues with a probable very large population and employment undercount in the household survey. These may be corrected in the CPS population controls - either in early 2025 or possibly as late as the 2030 Census. But they are unlikely to significantly shift the CPS ratios.