JOLTS Preview (January)

Fresh Data, Plus the Annual Revision

TL;DR: On Friday we get fresh data from JOLTS, providing useful updates on hiring and layoff trends in the first month of the year. We’ll also receive the annual revision to the historical JOLTS data.

This post covers:

The Big Picture

JOLTS Annual Revision

More below chart.

1. The Big Picture

The January monthly jobs report raised hopes that the labor market was on the verge of heating up again; the weak February jobs report brought us back to earth. In terms of timing, the JOLTS data sits between those two - turnover data covers the entire month of January and openings correspond to the final business day, whereas the jobs report data comes from early/mid-month.

The main question on my mind: what happened to hiring and layoffs during this period? Layoffs are a particularly intriguing case because we’ve gotten conflicting signals from job cut announcements (which have risen a fair amount over the past year, but I place less weight on) and initial claims (which I place more weight on, and have been very upbeat). If I had to bet, I’d guess that layoffs in January were very modestly higher than a year ago (less upbeat than claims, but much more upbeat than job cut announcements).

My base case for 2026 incorporates a slight decline in hiring and only a minimal (at most) increase in layoffs. So if that scenario proves to be correct, we should see only small changes on a month-to-month basis (abstracting from noise). But I’m not sure the base case is still operative; we’re in the middle (early stages?!?!?) of a war with negative (and potentially very negative) consequences for the labor market. An extended, unanticipated period of elevated energy prices is the kind of thing that would trigger further declines in hiring and an increase in layoffs. Let’s hope that doesn’t happen.

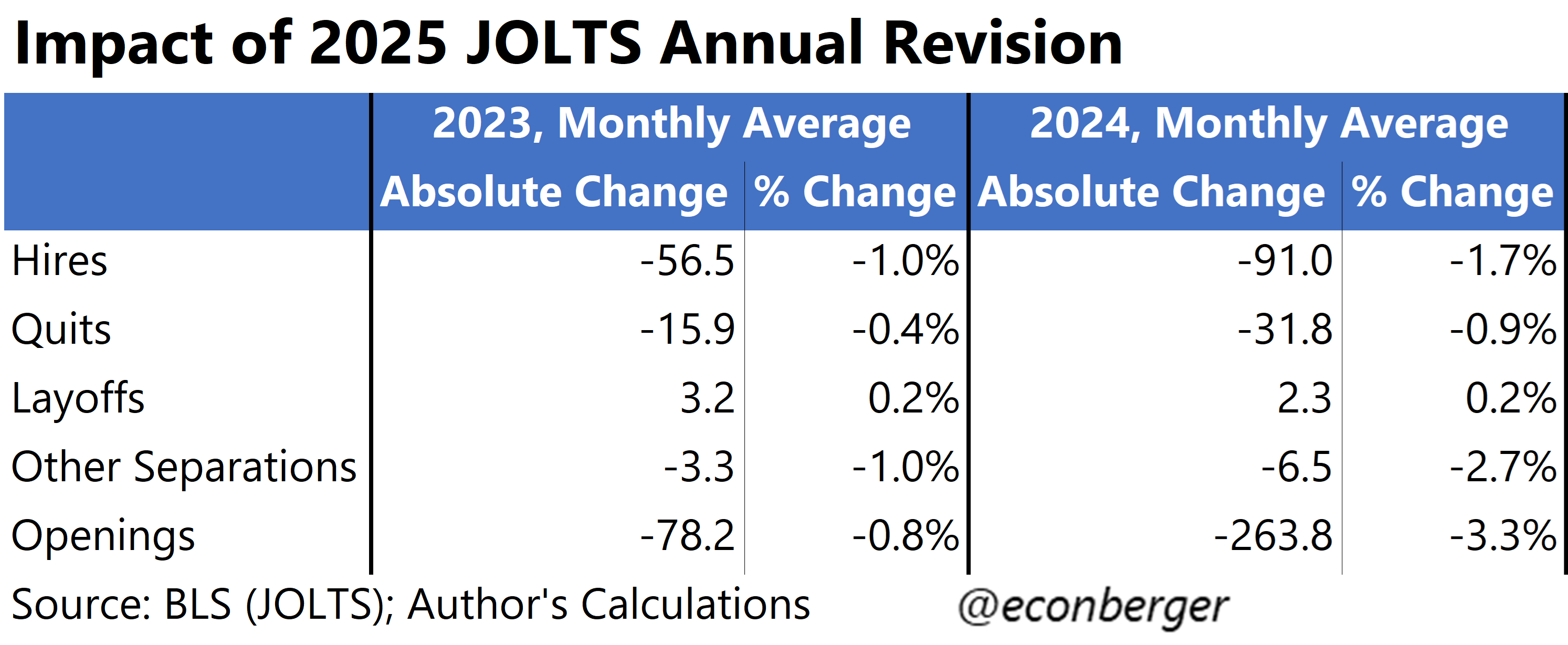

2. The Annual Revision

Every year the JOLTS data undergoes a revision to align itself to the Current Employment Statistics (CES establishing survey in the monthly jobs report).1 The CES underwent its own annual revision a few months ago, which led to very large negative downgrades to employment growth between March 2024 and March 2025 (due to the benchmark revision) and smaller downgrades to employment growth between March 2025 and December 2025.

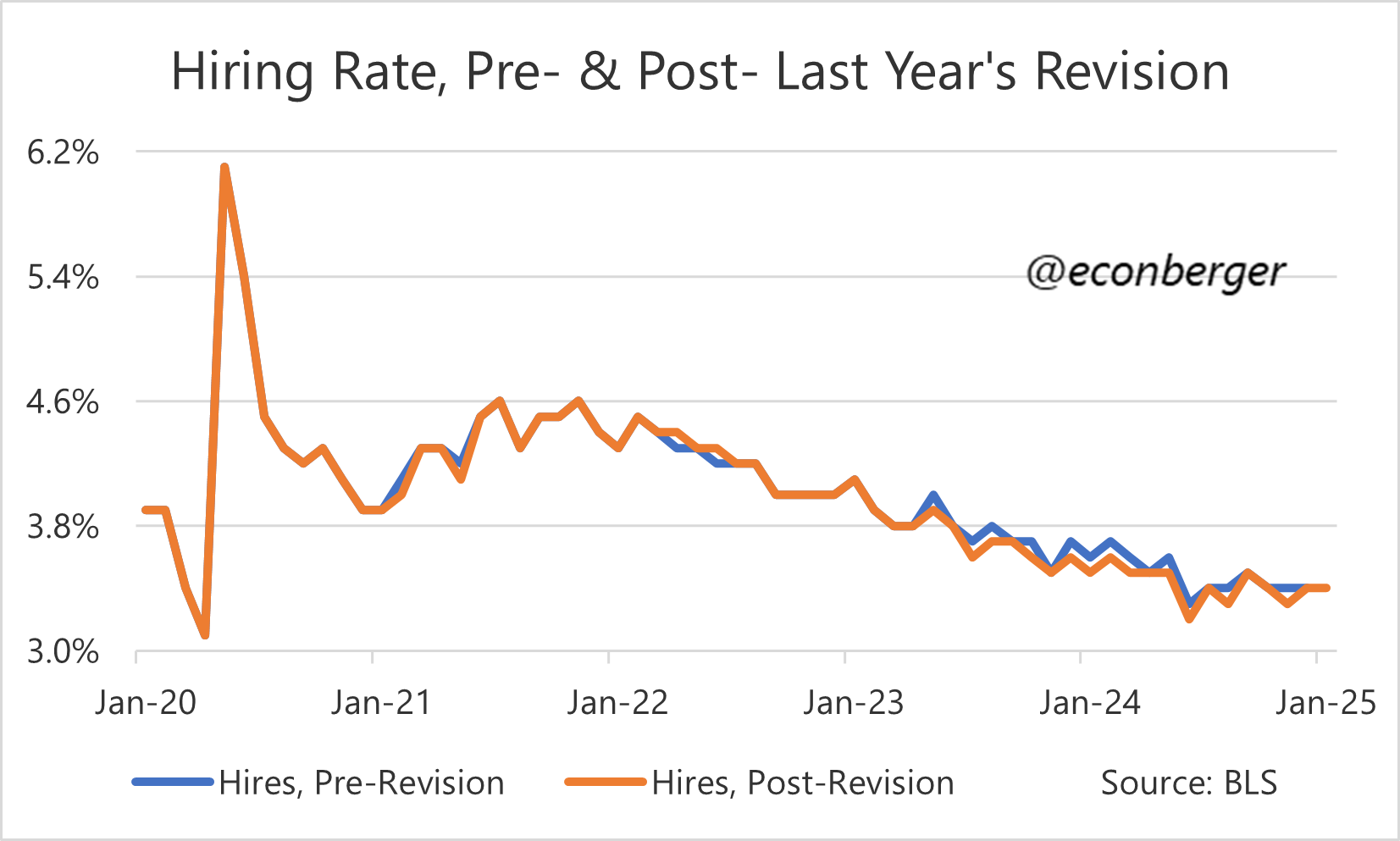

The main mystery in the JOLTS revisions is where those revisions will show up: lower hiring, higher quits or higher layoffs? Last year, when CES revisions were also large and negative, the impact came almost entirely via lower hiring whereas the upward revision to layoffs was minimal. I’d bet on a repeat of that pattern.

Before wrapping up the preview, I’d observe that these revisions, which seem dramatic when it comes to net employment growth, are much smaller as a portion of gross flows. 2024 hiring was revised down by 1.7% in last year’s revision - that’s enough to knock a tenth of a percentage point off some months’ hiring rate but not more than that. This year’s revision will be a little bigger, but I wouldn’t expect any big changes in the narrative of the past few years. It’ll end up being some combo of “Hiring a little weaker than we previously believed, which was already quite weak” and “Layoffs a little higher than we previously believed, but still quite low by historical standards”.

These revisions are the main reason the January JOLTS report is coming out on the 13th of March rather than the more typical 3rd or 4th. I would guess under-resourcing and ripple effects from the fall shutdown played a small role as well.