High Frequency Labor Market Indicators (7/01)

An Early Edition Ahead of Thursday's Jobs Report

TL;DR: Data in June was, on average, slightly softer than that in May.

This post covers:

Recent and Upcoming Posts

What’s Next

Policy Risks Update

Challenger Job Cut Announcements

Claims for Unemployment Insurance

Homebase

Indeed Job Postings

Morning Consult Unemployment Rate Index

ADP & Revelio Employment Growth

Revelio Turnover Metrics

Conference Board Labor Market Differential

Reading List

More below chart.

1. Recent and Upcoming Posts

On Thursday afternoon I’ll publish a recap of the June jobs report. You can read my preview of the report as well as a recap of the May JOLTs data.

If you’re interested in my more thematic work, here’s an assessment of the most upbeat labor market indicator in America and a comparison of hiring vs. job finding rates. And I’m cooking up a piece on layoffs and hiring across tech sub-industries, which will come out “in a few weeks”.

I’m also posting on the Access/Macro newsletter, where I wrote about the emerging pattern of upward revisions to nonfarm payrolls data. If you’re interested in what else I’m up to, Homebase just published their June Main Street Health Report; last week Guild published their June Workforce Signal - it’s about how curriculum choices have changed during the labor market freeze.

2. What’s Next

Labor markets go back into hibernation next week; we’ll probably get claims for unemployment insurance, Morning Consult, ADP and Indeed, but little else. Further ahead, recent discourse about wage growth has me looking ahead to the July 31st release of the Q2 employment cost index. And because we’re talking a lot about creative destruction these days, I’ll check out the Q4 2025 Business Employment Dynamics data on July 29th. Finally, we get the Q1 2026 QCEW data on August 28th, and presumably a preliminary benchmark announcement the same day.

3. Policy Risks Update

Hormuz traffic continues to gradually normalize. For more on the topic of the Iran conflict and its impact on energy prices, I recommend following Rory Johnston and Gregory Brew. Otherwise I don’t see any big policy risks pertaining to the labor market, aside from monetary policy turning hawkish.

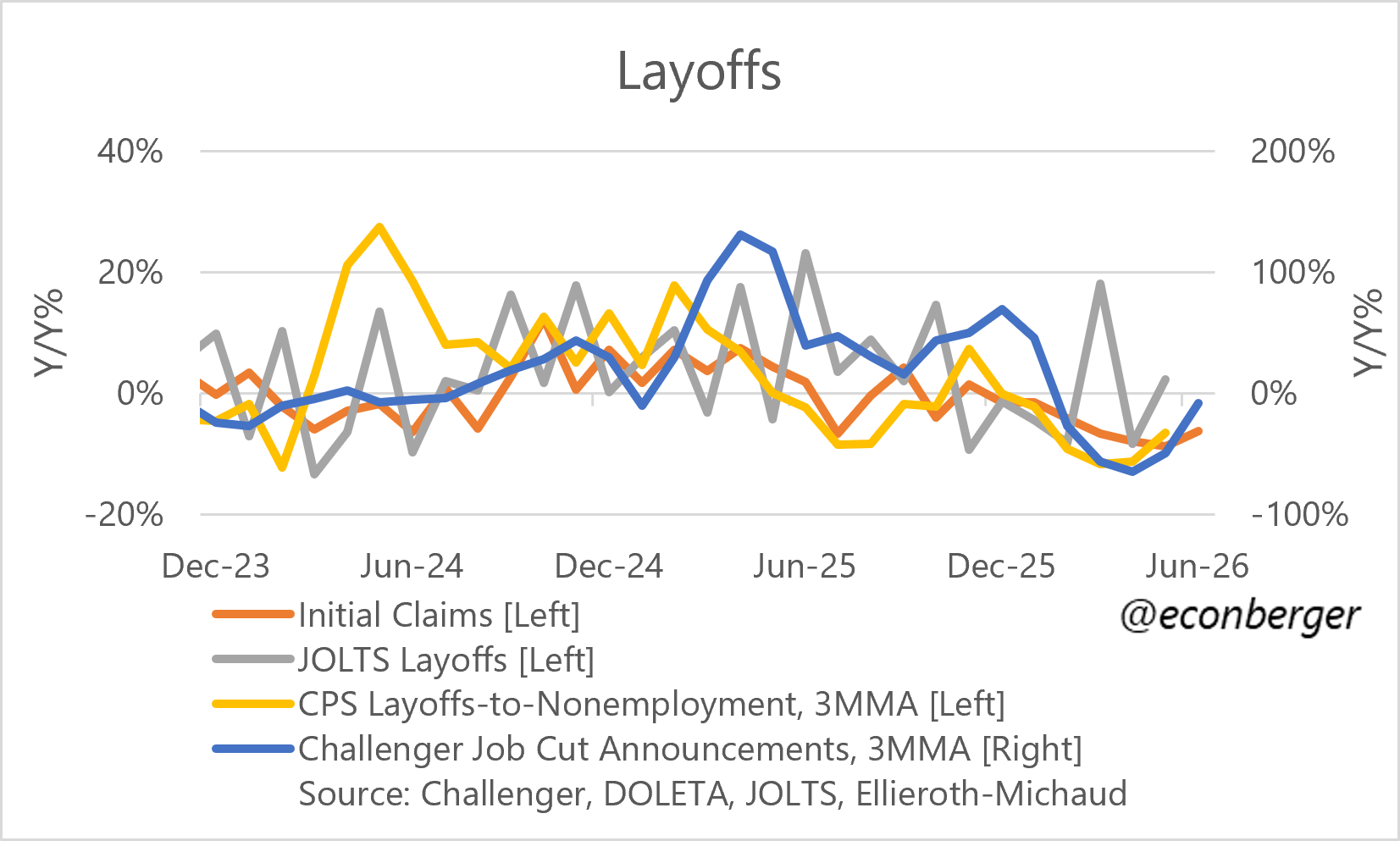

4. Challenger Job Cut Announcements

This former doomer darling continues to signal lower layoffs than a year earlier (just like higher quality indicators), though the decline is tapering off.

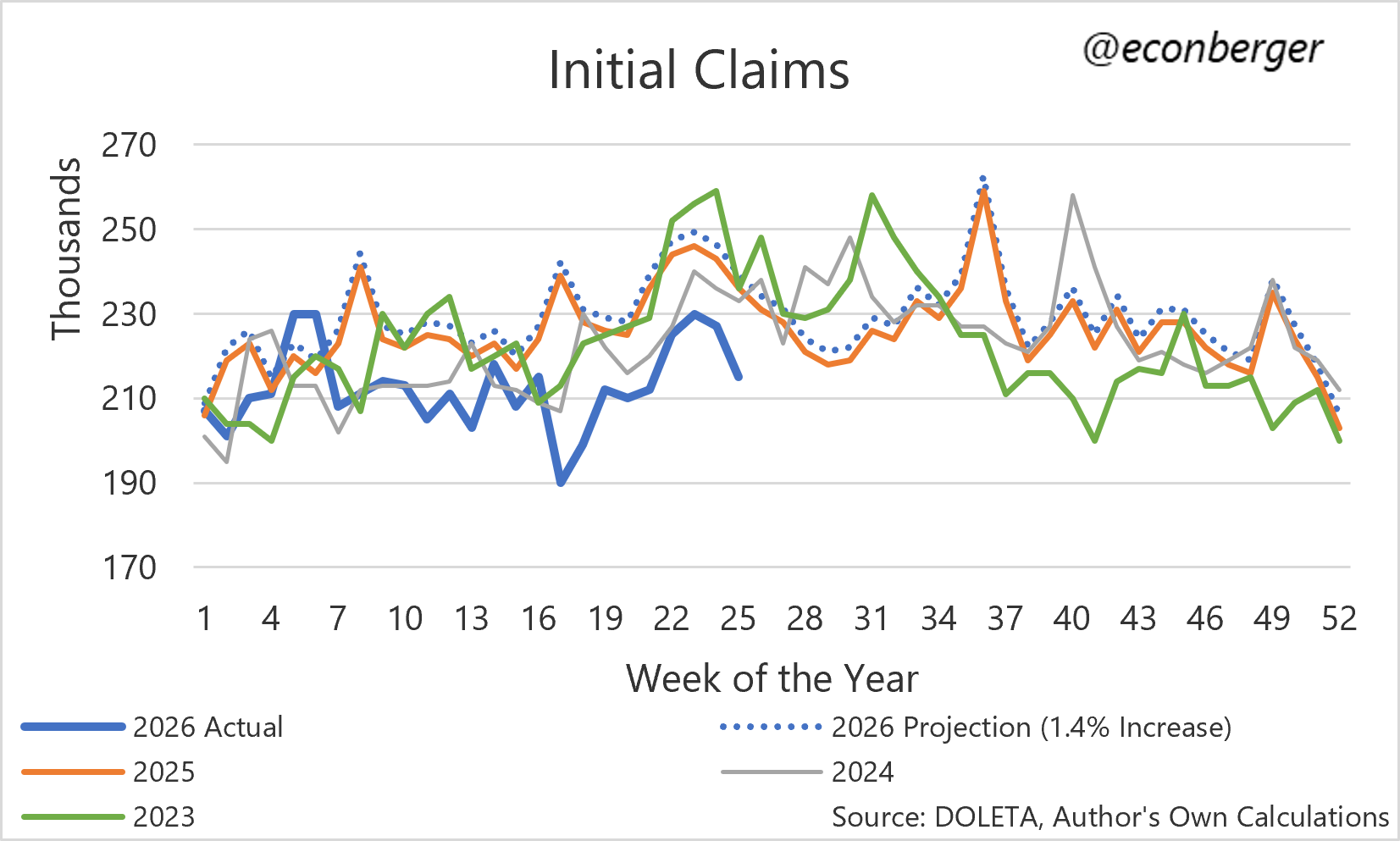

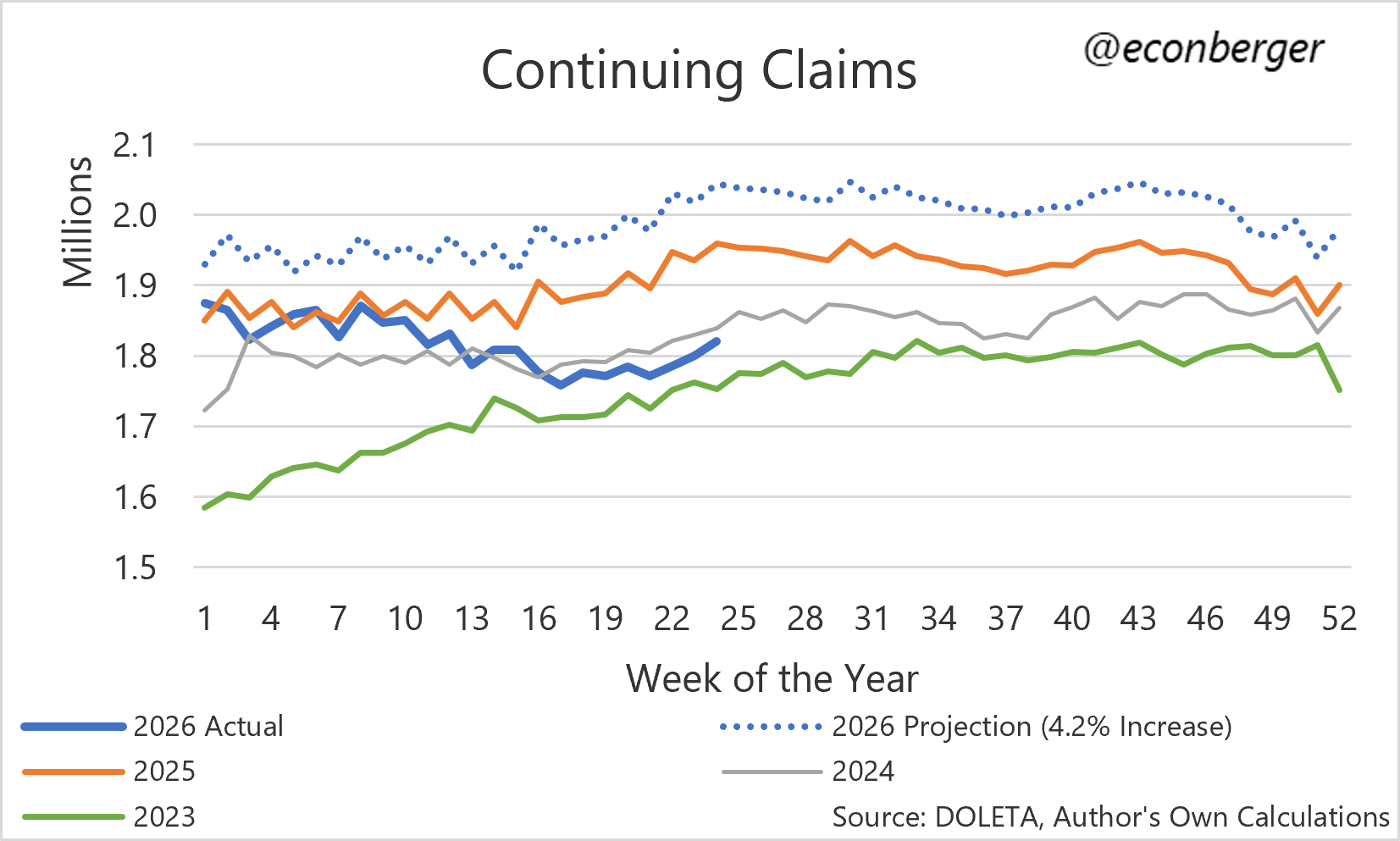

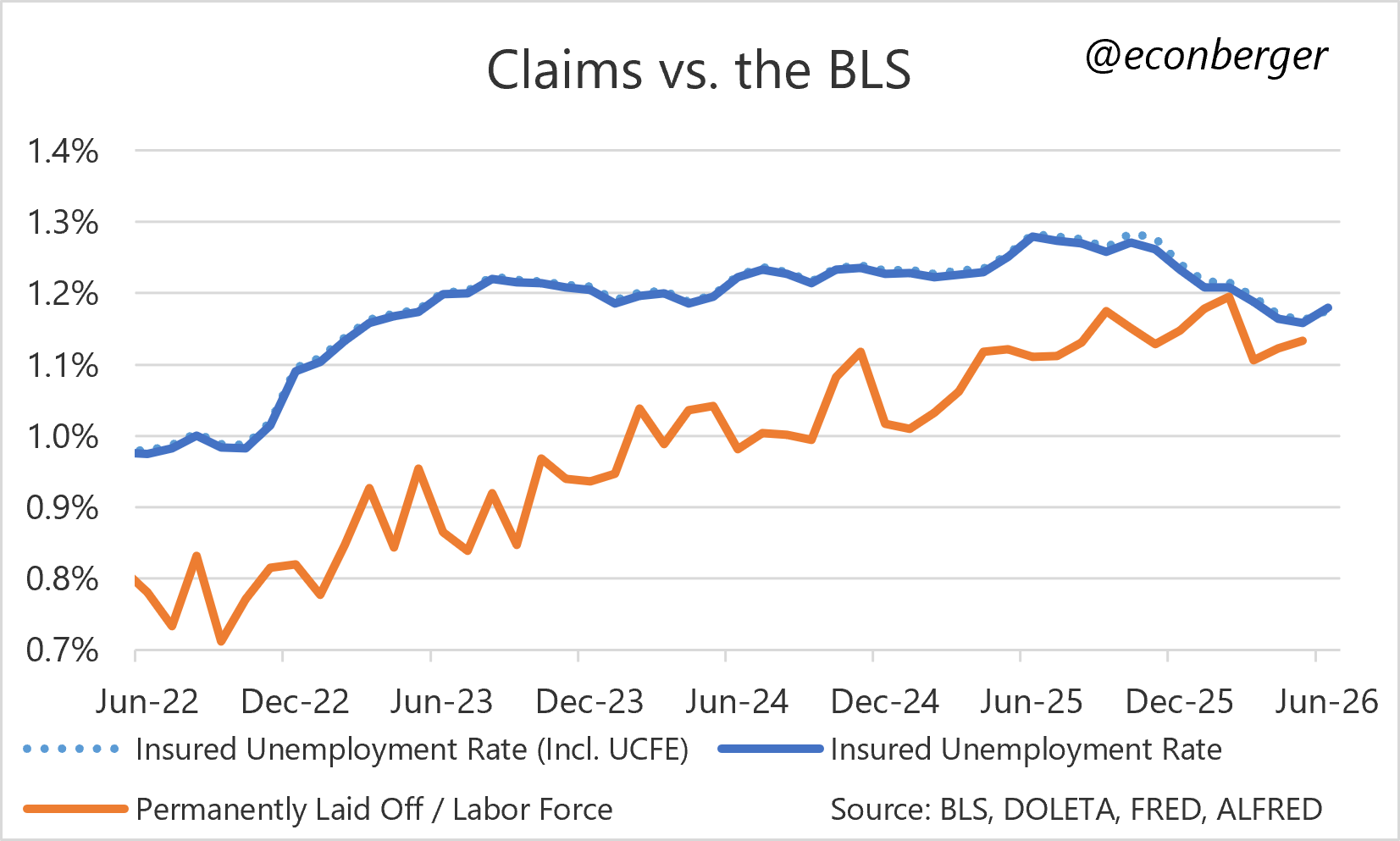

5. Claims for Unemployment Insurance

We don’t have new claims data ahead of the BLS release (since the jobs report is being released on Thursday at the same time), but below I’m reproducing the charts from last week. Initial and continuing claims have both increased in June relative to May, but I think this is probably residual seasonality. The insured unemployment rate continues to signal a flat “unemployment rate due to permanent layoff”.

6. Homebase

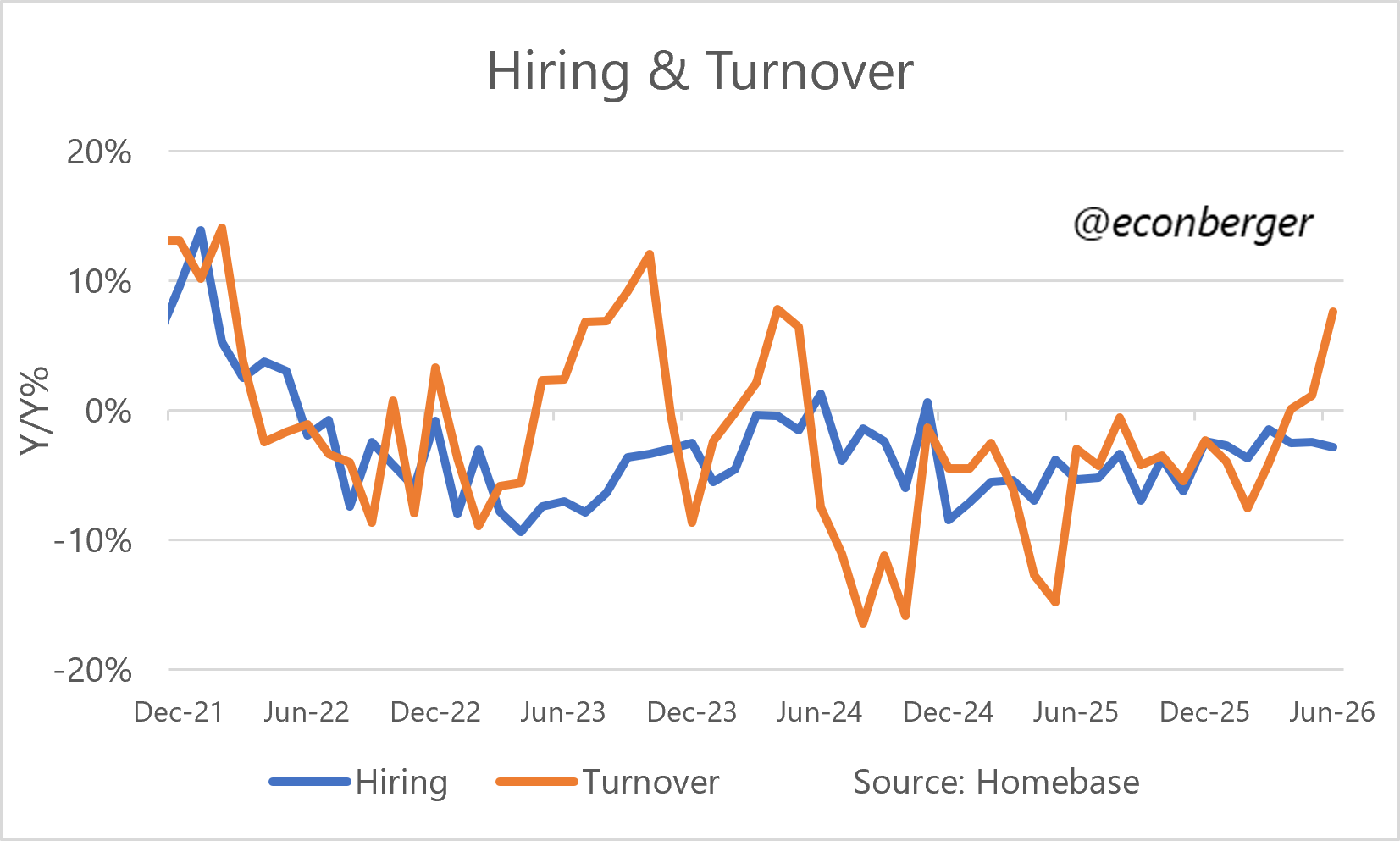

I am Homebase’s Chief Economist, and in June we saw a big spike in turnover (+7.6% Y/Y). Hiring was still down a little (-2.8% Y/Y). I’m pretty sure the June turnover surge will unwind, but the more modest increase in turnover we saw in April and May is probably more durable.

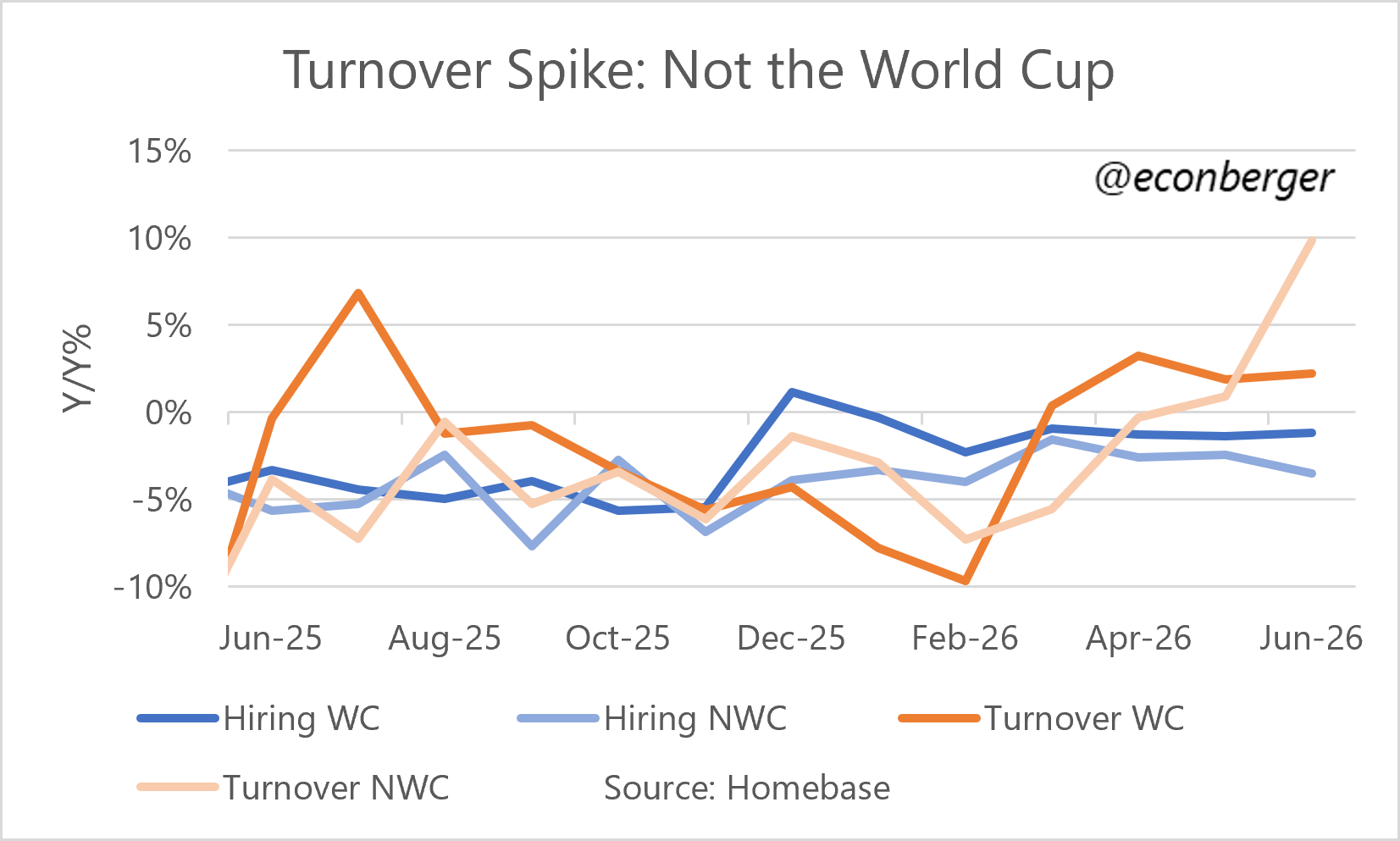

One thing we were curious about: how much of this is the World Cup? And I’m inclined to answer, a little at most. It really is the case that hiring is falling more slowly in the 11 World Cup hosting cities than elsewhere, but this outperformance began late last year. And the June turnover surge happened entirely outside of the 11 host cities; in the 11 host cities, turnover growth has not budged recently.

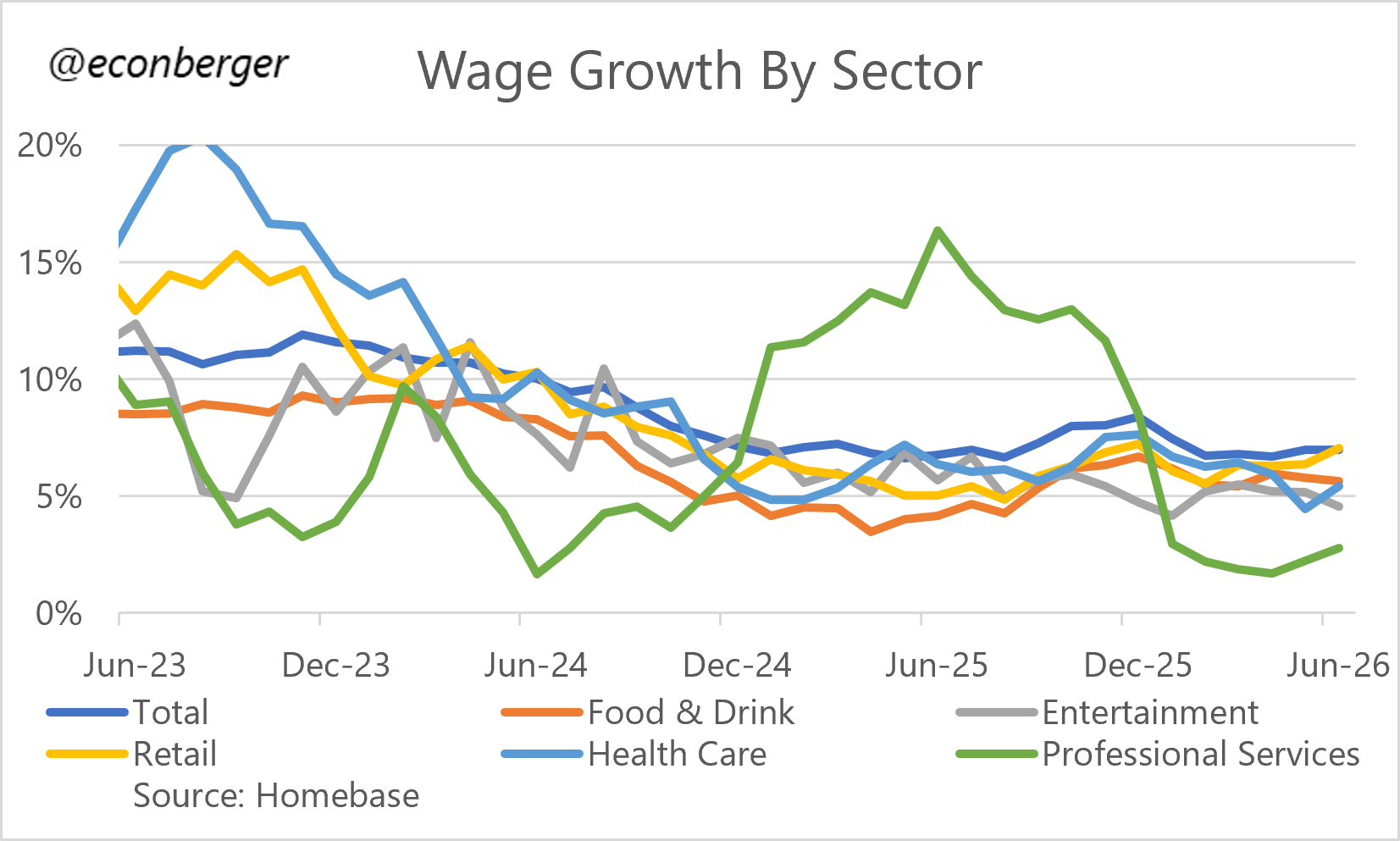

Finally, wage growth has been fairly stable of late:

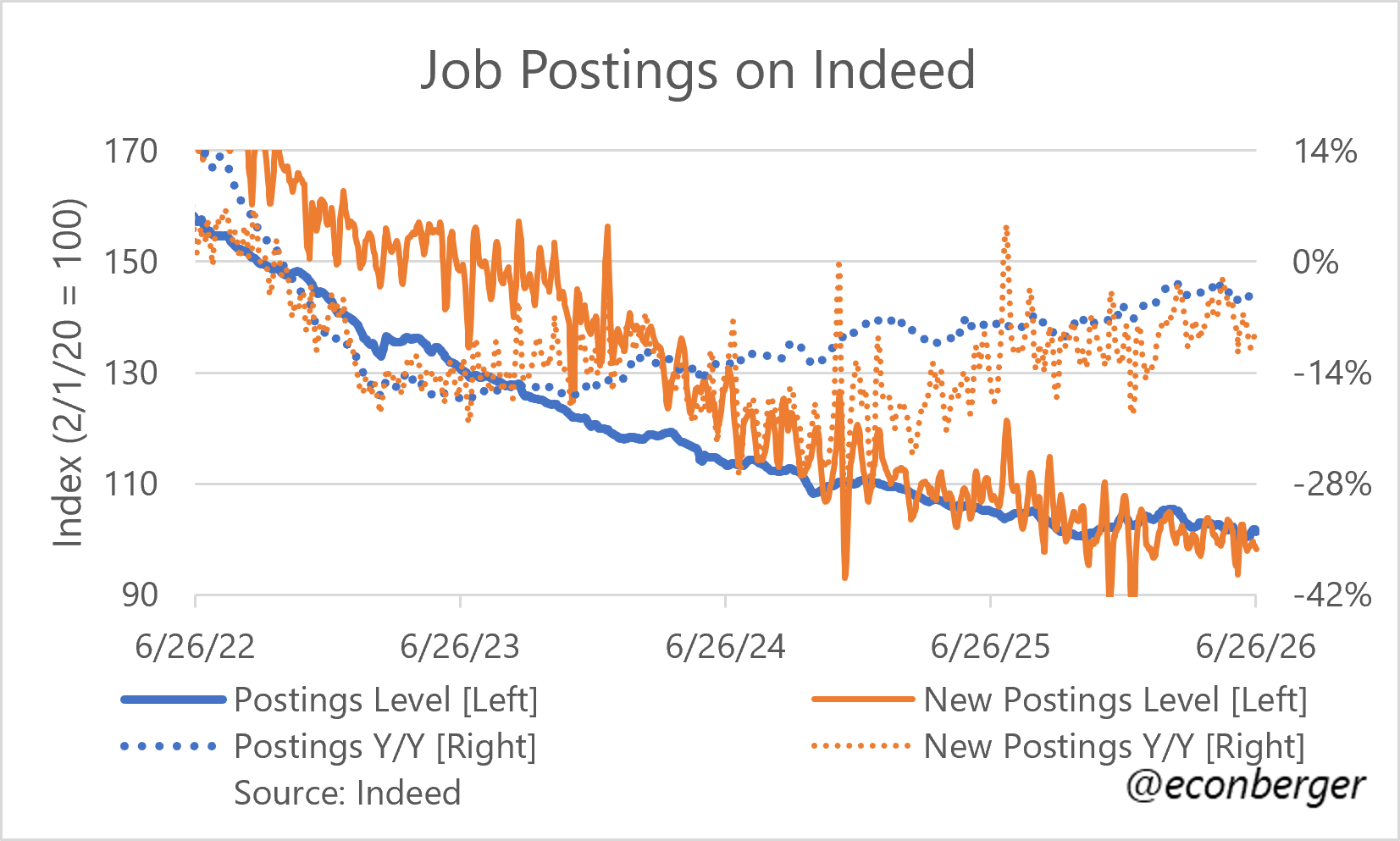

7. Indeed Job Postings

Indeed job postings had a weak end to May, and a weak start to June. Since then, they’ve regained some strength, but remain below year ago levels. The most optimistic take is that they’re stable (in levels, since last fall); we’re not seeing any signs of a recovery, much less a boom.

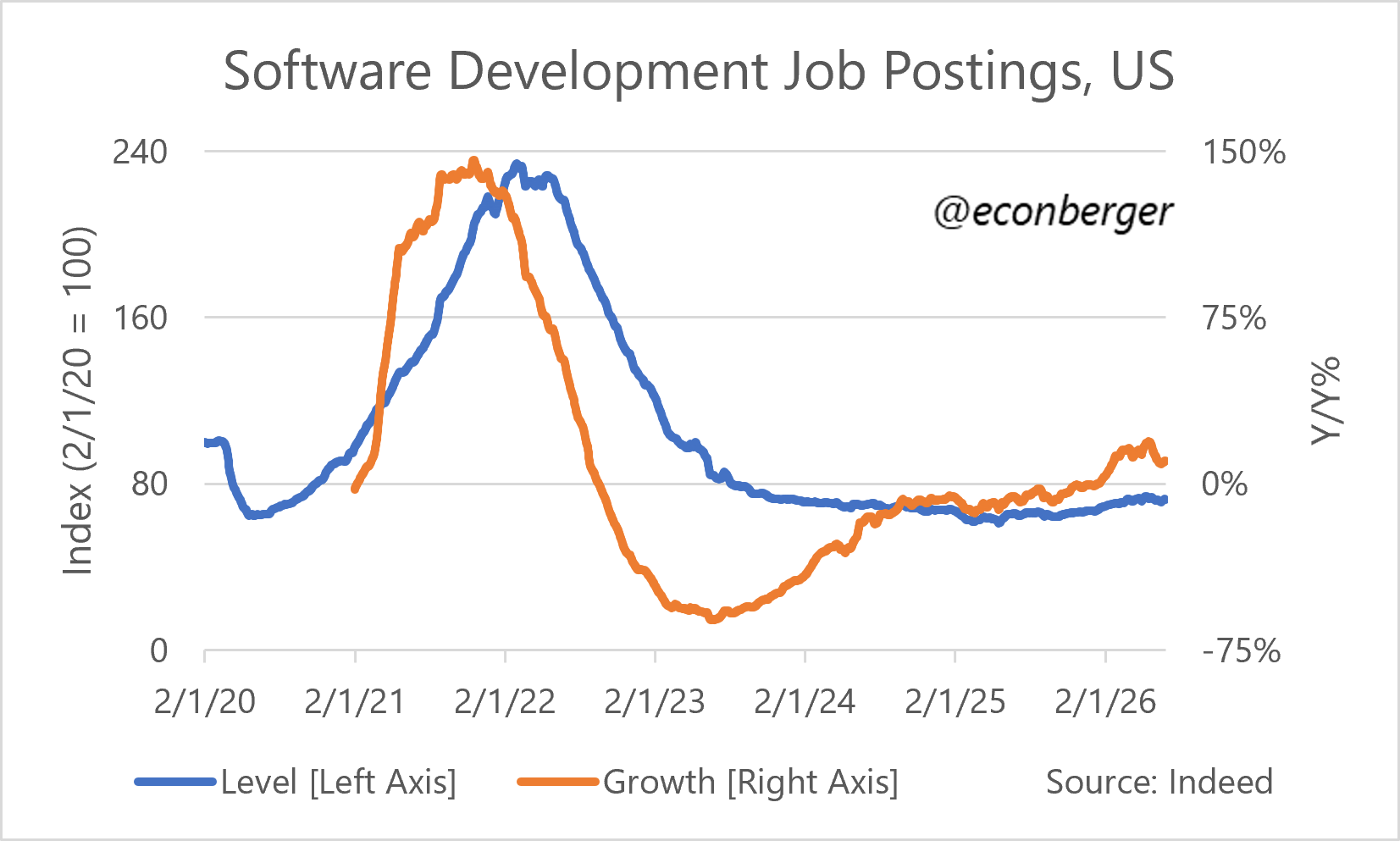

Software development postings, which were growing very rapidly earlier in the year, experienced a sharp deceleration in June.

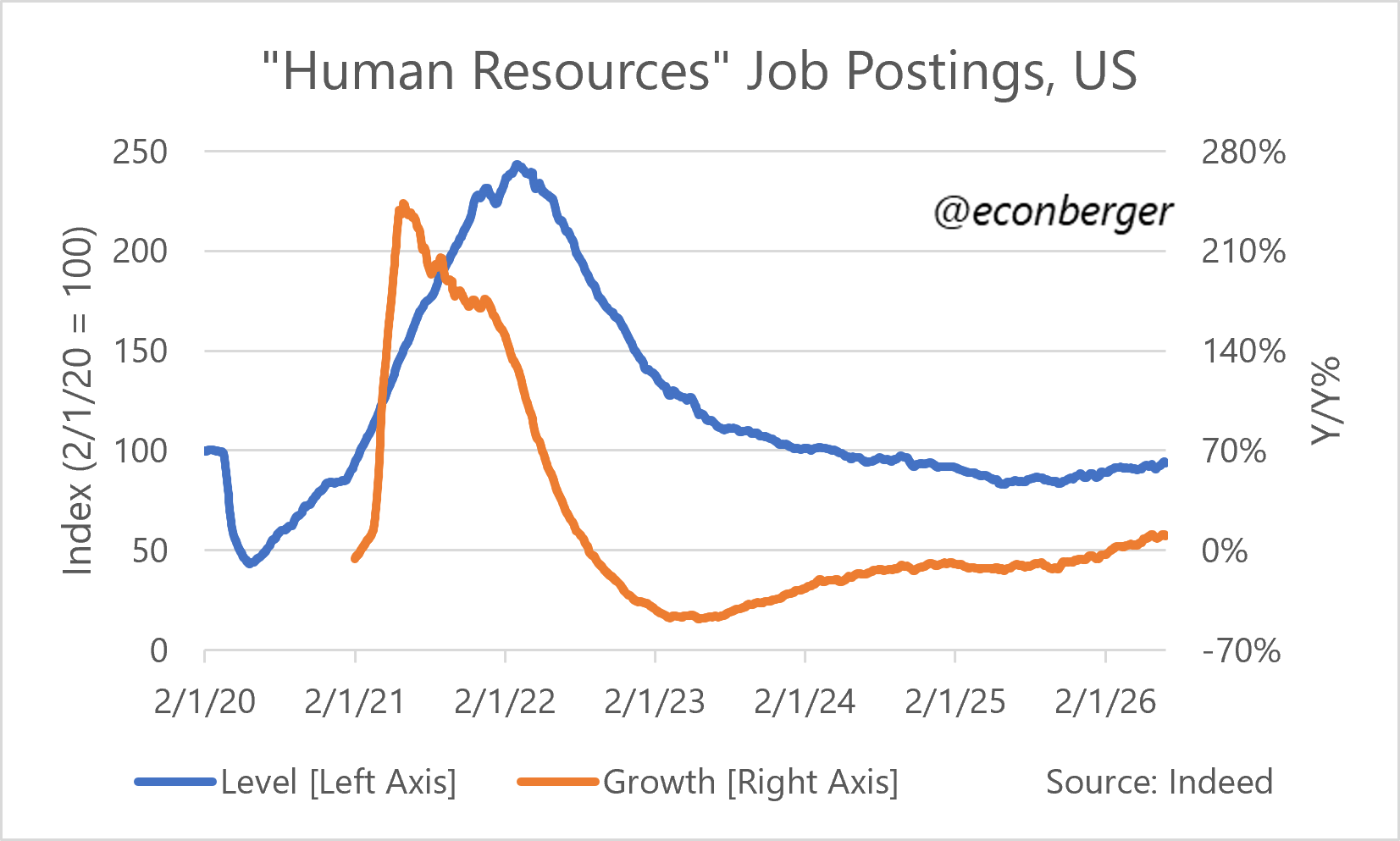

And “human resources” postings, which include recruiting roles and have been a messy/unreliable/occasional leading indicator for overall postings, have continued to grow at a solid pace:

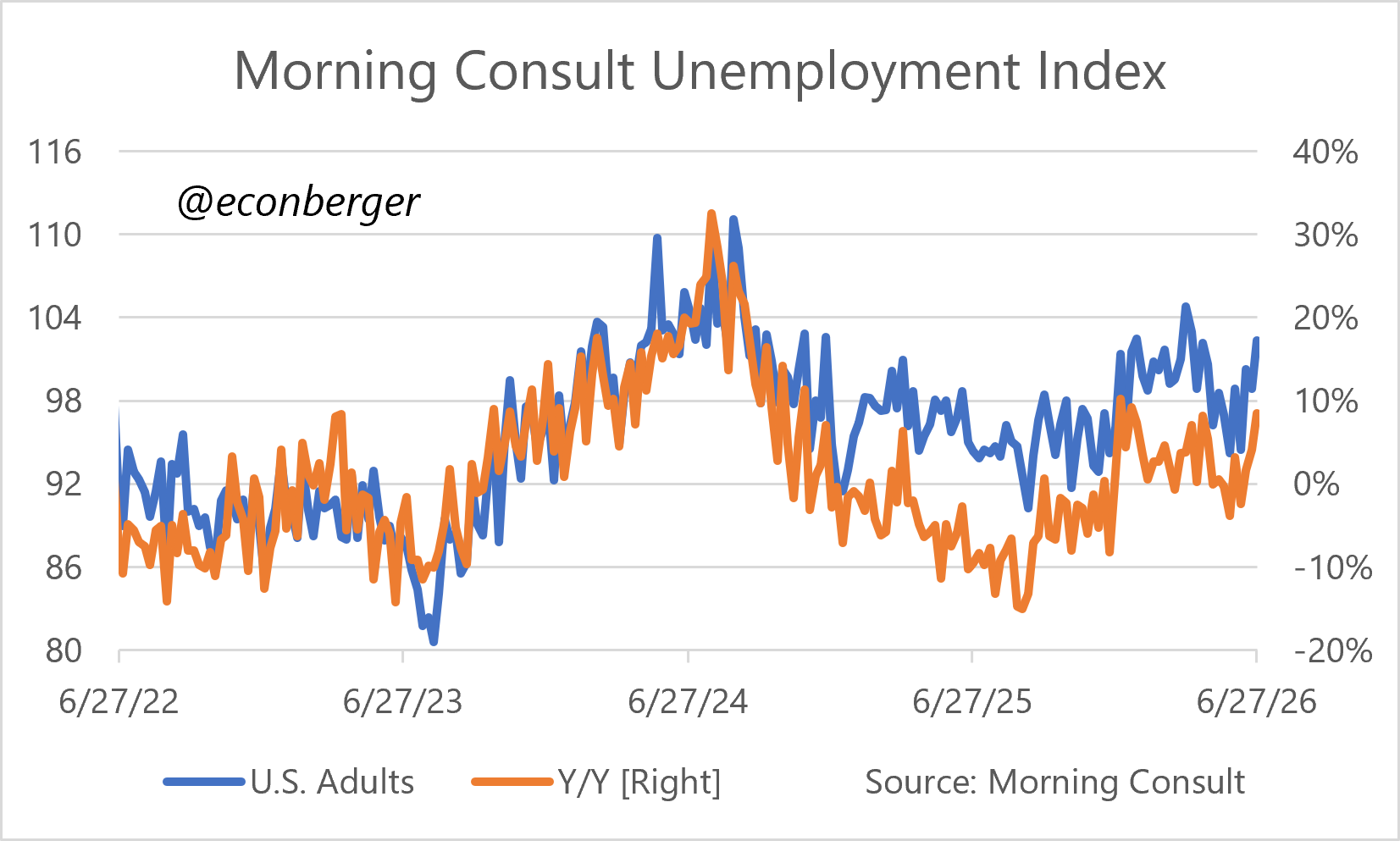

8. Morning Consult Unemployment Rate Index

The Morning Consult unemployment metric, which applies the BLS definition to Morning Consult’s own survey, has looked worse in June than it did in May.

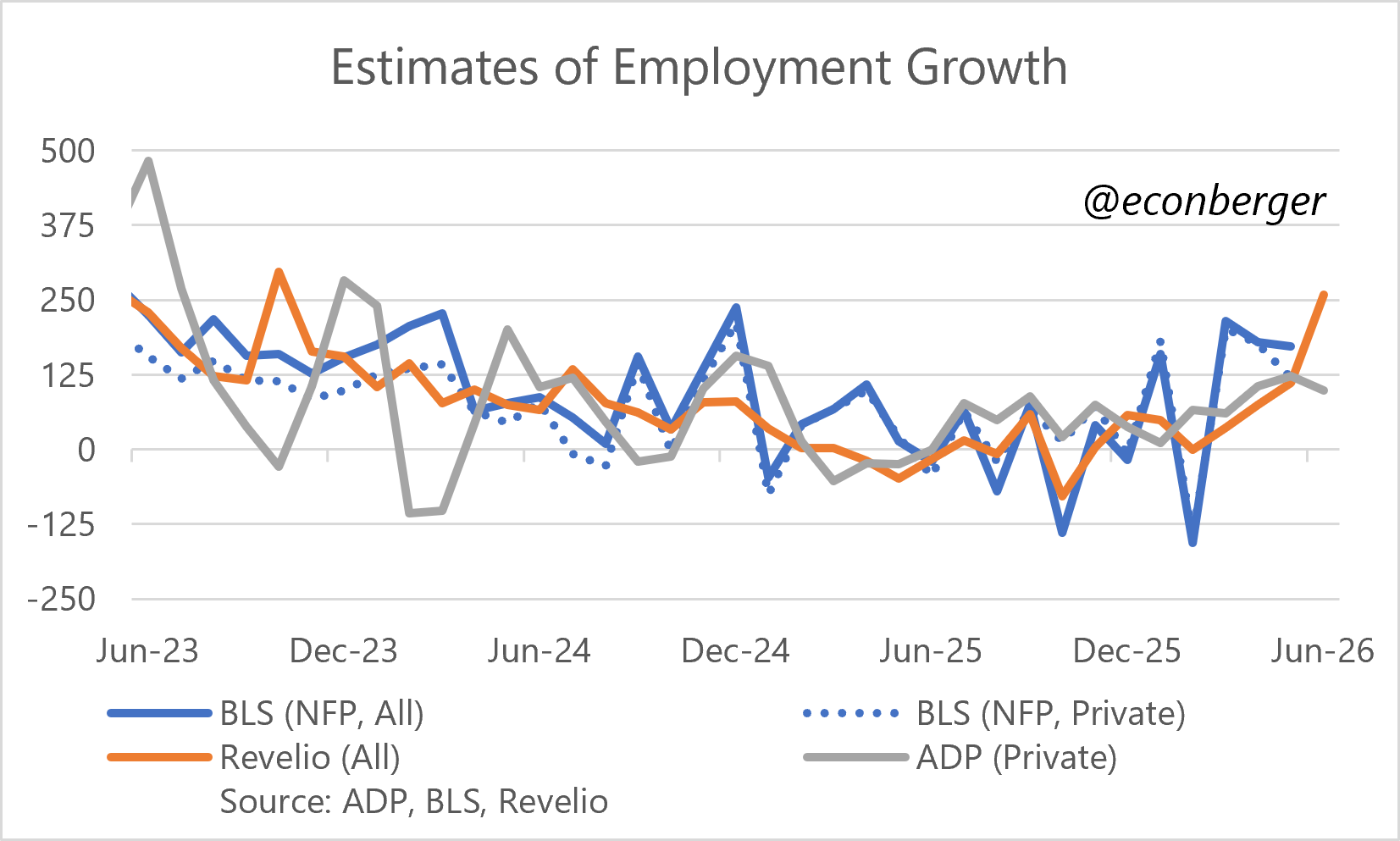

9. ADP & Revelio Employment Growth

ADP and Revelio both produce estimates of employment growth. Both agreed that it was positive in June, but wildly disagreed on the magnitude. ADP had an increase of +98K, a solid number but lower than last month; Revelio’s +259K was the strongest estimate they’ve had in a long time. I think ADP is likely much closer to the June BLS number, but in the unlikely case that Revelio is right, it would be a huge feather in their cap.

10. Revelio Turnover Metrics

Revelio’s turnover metrics, based on LinkedIn data, are among the most valuable items in their dataset. They provide an explanation for why Revelio’s net employment growth estimate is so positive: separations plunged in June, according to their estimate. Their measured increase in hiring was very small.

11. Conference Board Labor Market Differential

I don’t have a chart for this indicator since I don’t have access to it, but it worsened in June. This is now one of the most consistently downbeat labor market indicators, but also one that seems increasingly out of touch with the hard data.

12. Reading List

I didn’t read anything on the list last week, but at least it didn’t get longer!

“How Will AI-driven Automation Actually Affect Jobs?” by Alex Imas and Soumitra Shukla

“Weak Bundle, Strong Bundle” by Luis Garicano , Jin Li, and Yanhui Lu

“Inflation Inequality Meets the Great Wage Compression” by Arin Dube

“The Cross-Section of Non-Citizens and the Jobs Slowdown” by Mike Konczal

“Making Sense of Labor Market Indicators Amid Data Imperfections” by Aysegul Sahin, Bart Hobijn, Scott Brave, Erin Crust and Stefano Eusepi