JOLTS Recap (May)

Can the (Very Small) Hiring Thaw Persist?

TL;DR: We’re seeing a modest improvement in hiring; that improvement, coupled with a small decline in layoffs, has powered faster employment growth and a slight decline in the unemployment rate.

This post covers:

The Big Picture

Data Roundup

More below chart.

1. The Big Picture

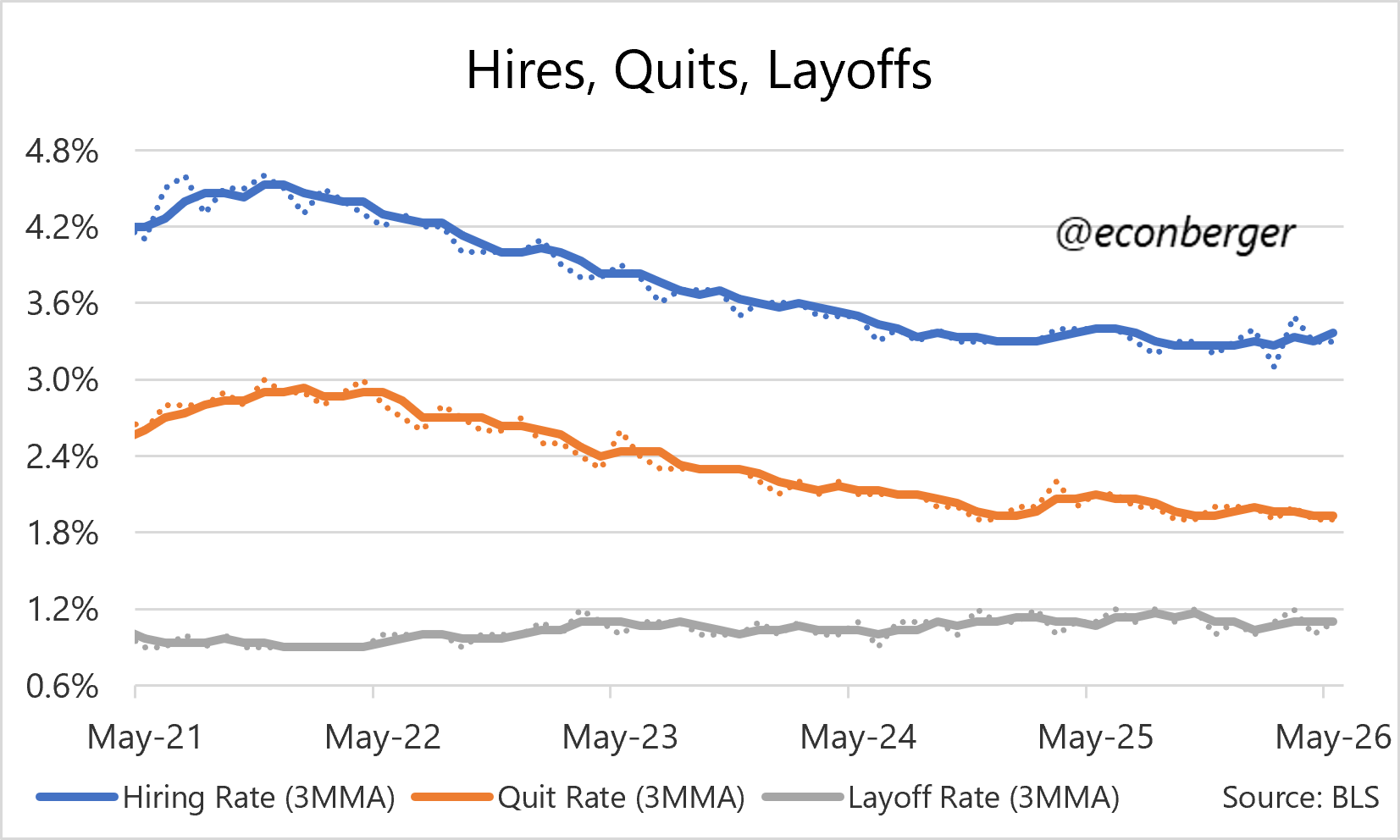

The job market has warmed slightly in recent months, and if you squint hard enough, you can see it in the JOLTS data. You really do have to squint: the hiring rate has averaged 3.32% in the first 5 months of 2026, vs. 3.27% in the final 6 months of 2025. Normally I’d be dismissive of such a tiny shift as a blip. But I think it’s real rather, because we’ve seen a small improvement in the labor market across a wide range of data sources.

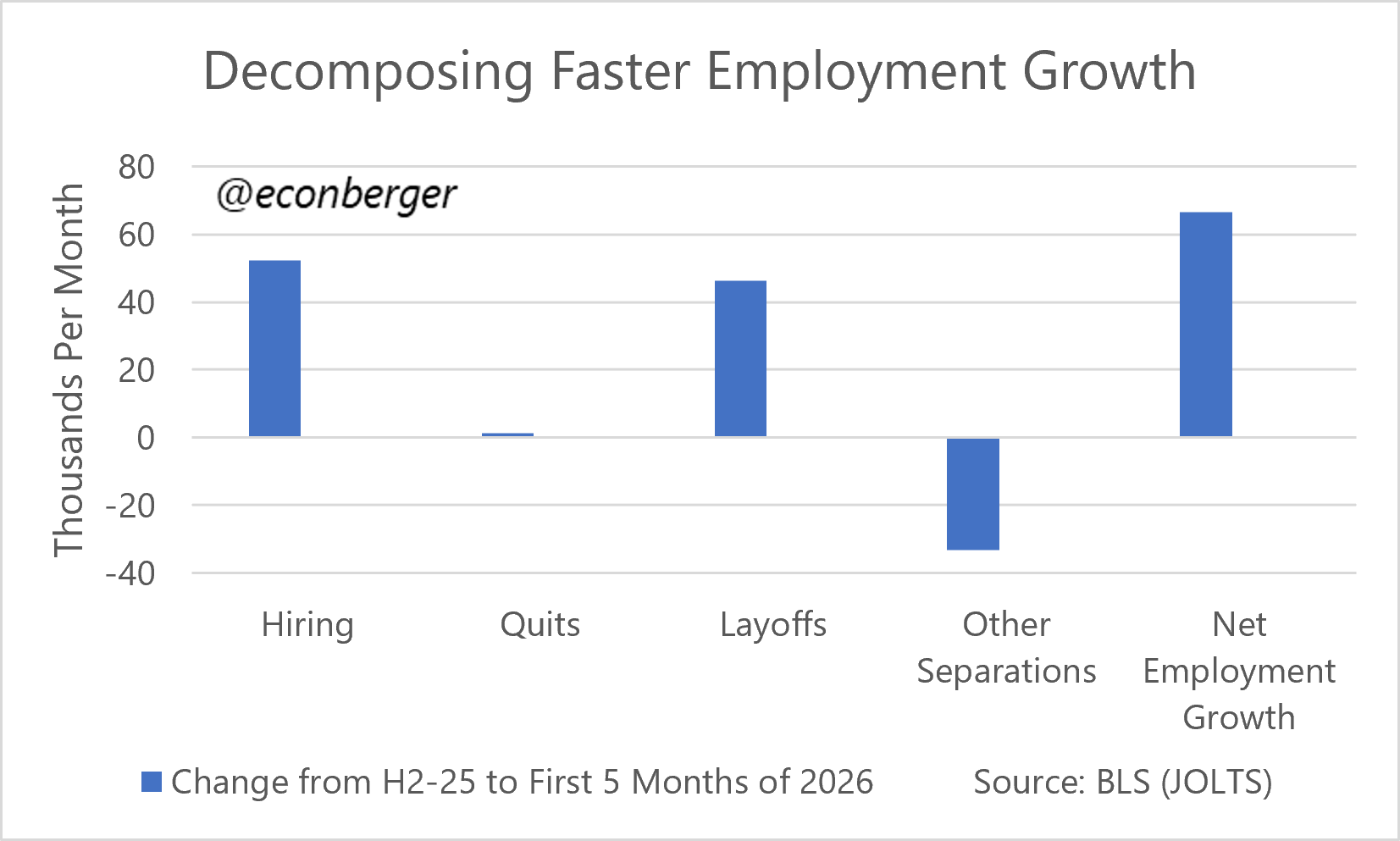

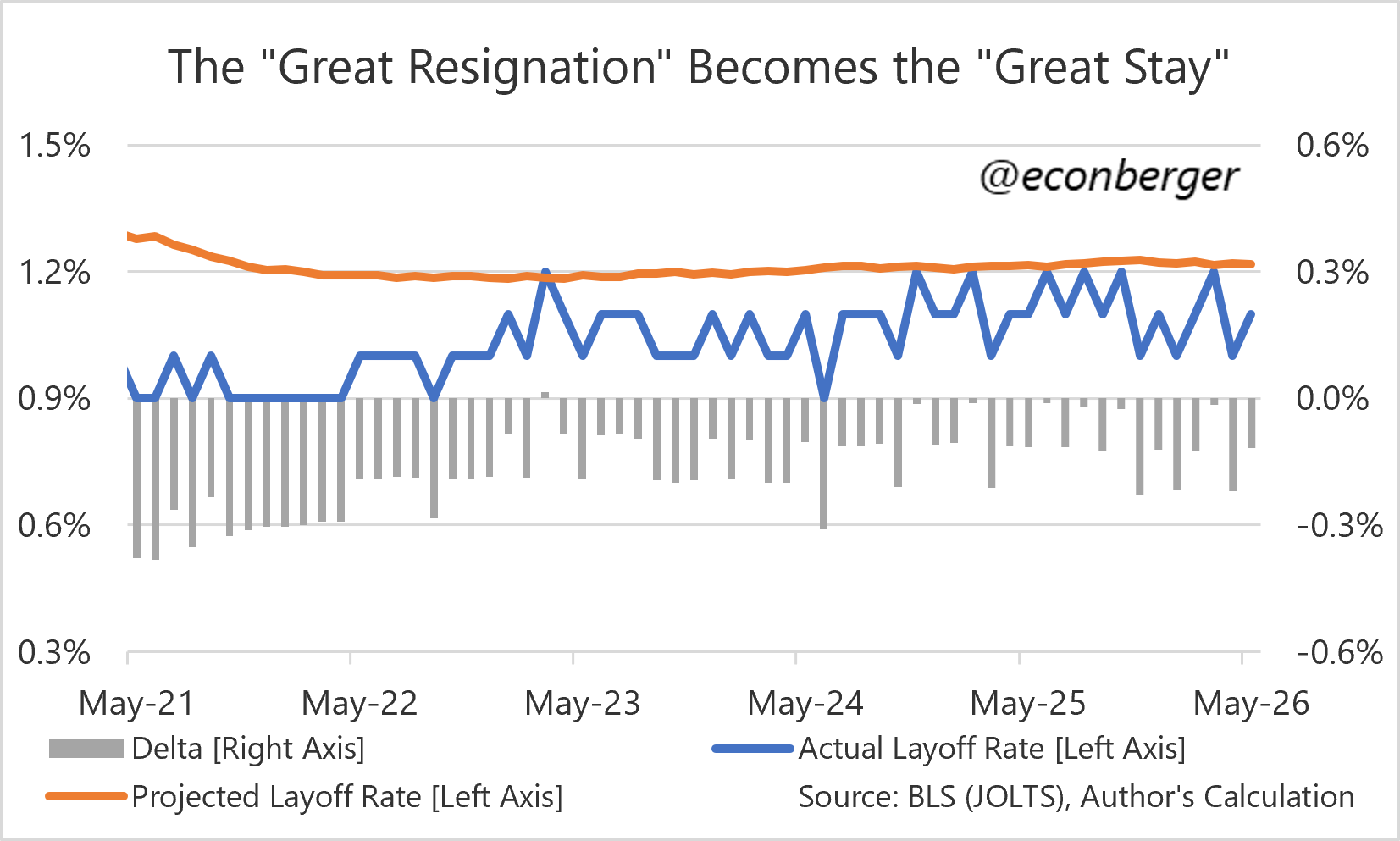

There’s also been a small decline in the layoff rate over the same period (1.08% vs. 1.12%). Hiring has increased by 1.0%; layoffs have declined by 2.6%. We’ve crossed over from “slow labor market cooling” to “very slow labor market warming”, which feels like a bigger deal than it actually is. On the current trajectory, it will take a very long time for the labor market to unwind the meaningful but not-that-large damage incurred in 2023-25.

I’m not sure whether this very mild warming will persist, much less intensify. At this point I’m informally attributing it to spillover from equity prices; these are encouraging businesses to hire more people, and consumers to spend more money. Barring a sudden reversal in the stock market, we have at least a little more upside.

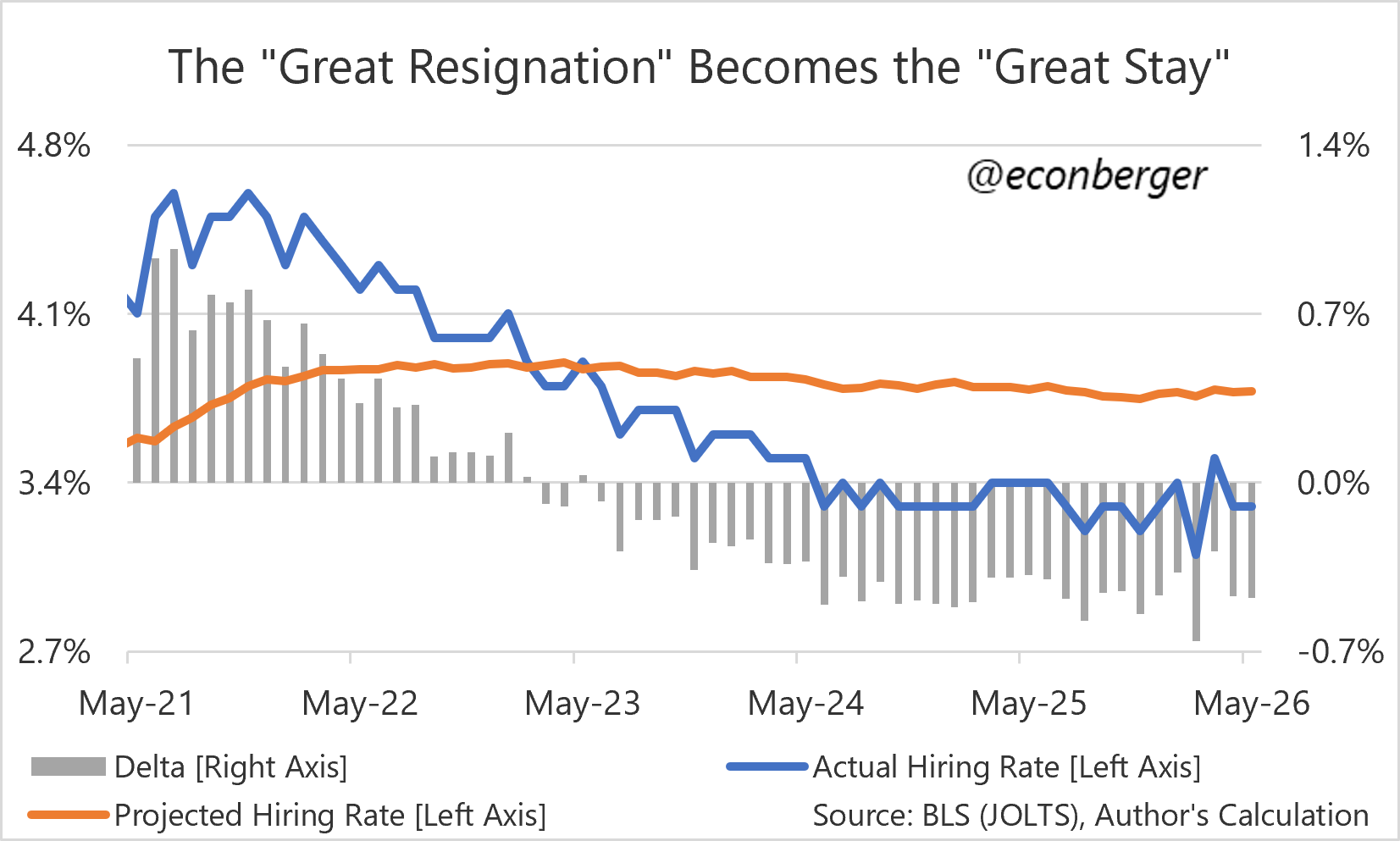

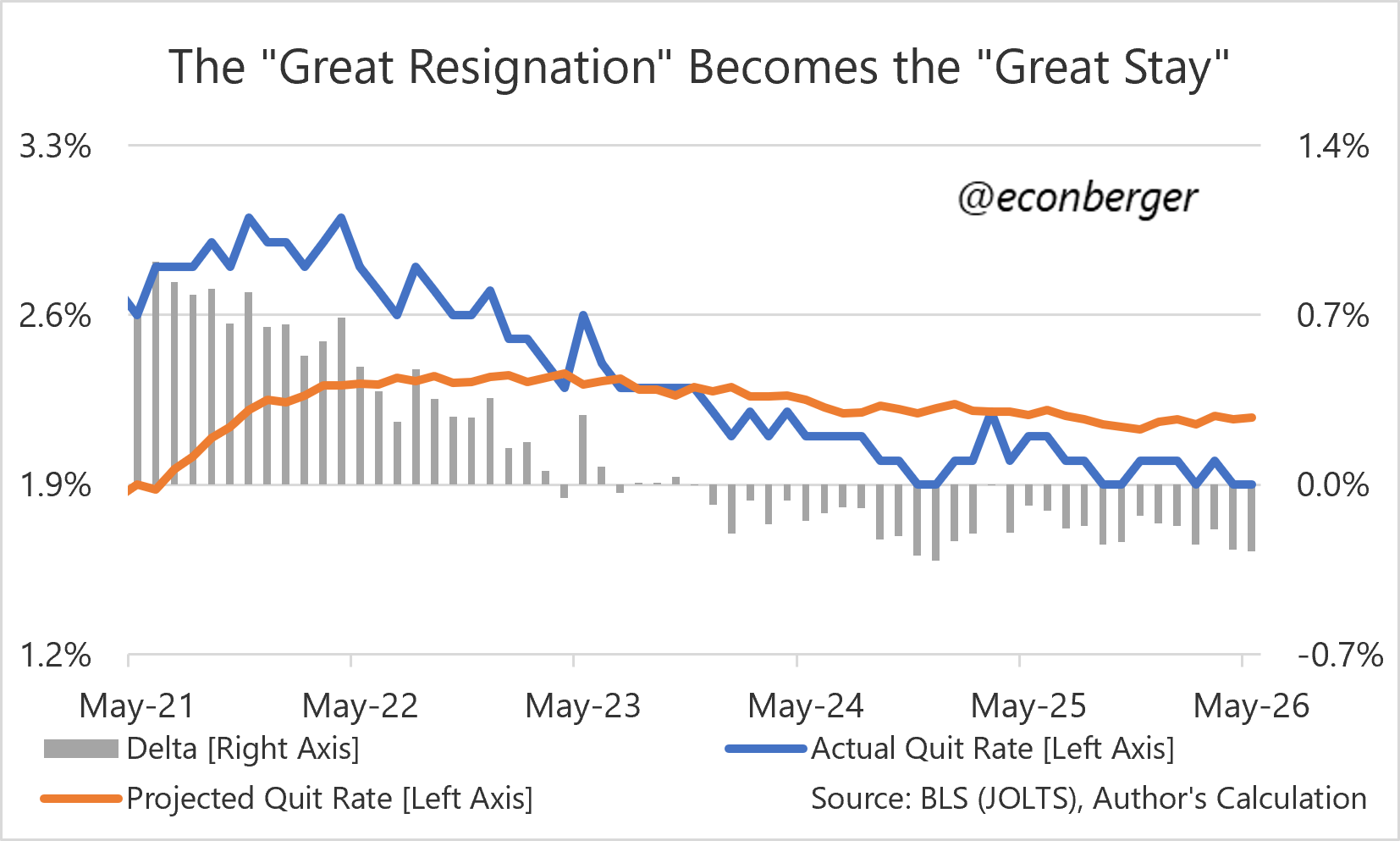

If it the warming does continue and/or intensify, I’d expect any further increases in hiring to be accompanied by an increase in quits. So far quits haven’t budged! But workers will take more chances if they see further growth in outside opportunities.

A final point before I move onto the data roundup. “Other separations” have increased this year; these could be higher retirements though we can’t be sure. Either way, they’re creating space for higher hiring and lower layoffs.

2. Data Roundup

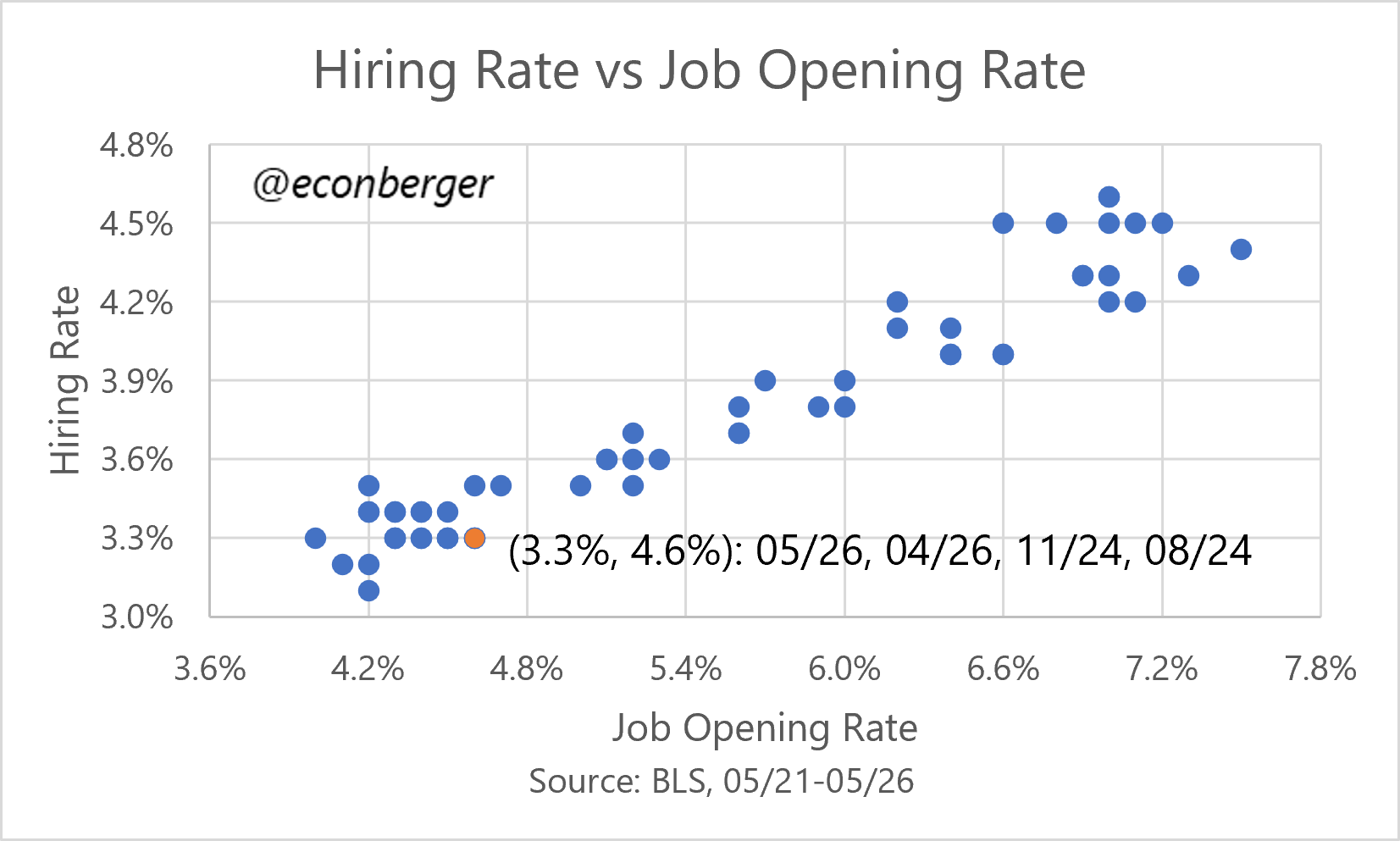

As I said above, the increase in hiring this year (relative to H2 2025) has been very small, even if real. It hasn’t been enough to change an essential characteristic of today’s job market: it’s still really hard to find a job. June’s hiring rate of 3.3% was comparable to what we saw in the early 2010s, around the time when the unemployment rate was 8%.

Quits are also a little on the low side, and as I stated earlier, have not matched even the very small improvement seen in hiring and layoffs. June’s quit rate of 1.9% is a mid-2010s-style number; back then the unemployment rate was around 5.5%.

And layoffs remain very low by historical standards. If you have a job, in most sectors you’re as secure as you’ve ever been.

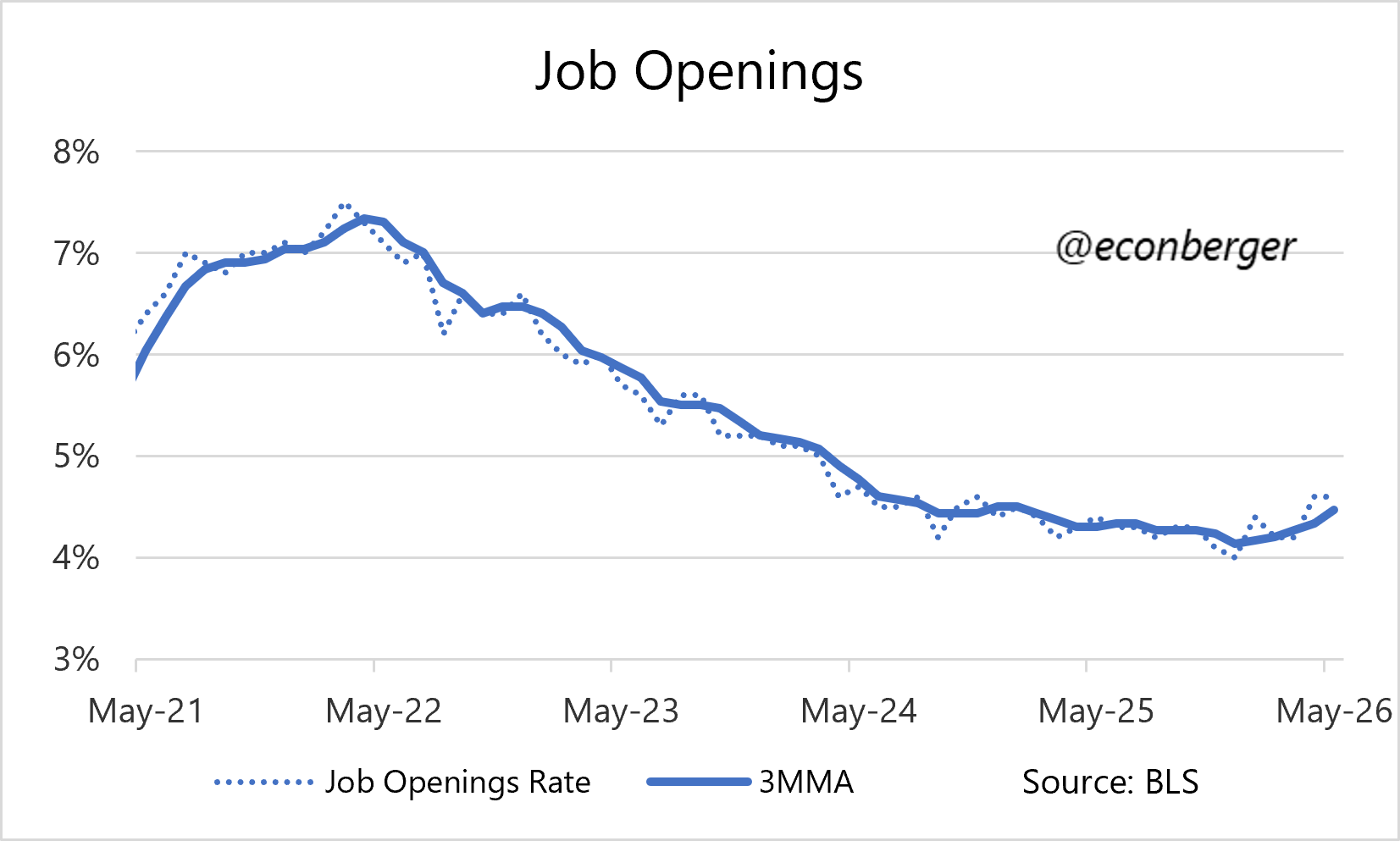

Something that has gotten people excited: what looks like a small uptrend in job openings. I’m not certain it will persist, given that we haven’t seen a comparable improvement in the Indeed job postings data. But even if it sticks, it’s consistent with the modest hiring increase I talked about it earlier; there’s no reason, based on what we’ve seen in openings, to expect a big increase in hiring.1

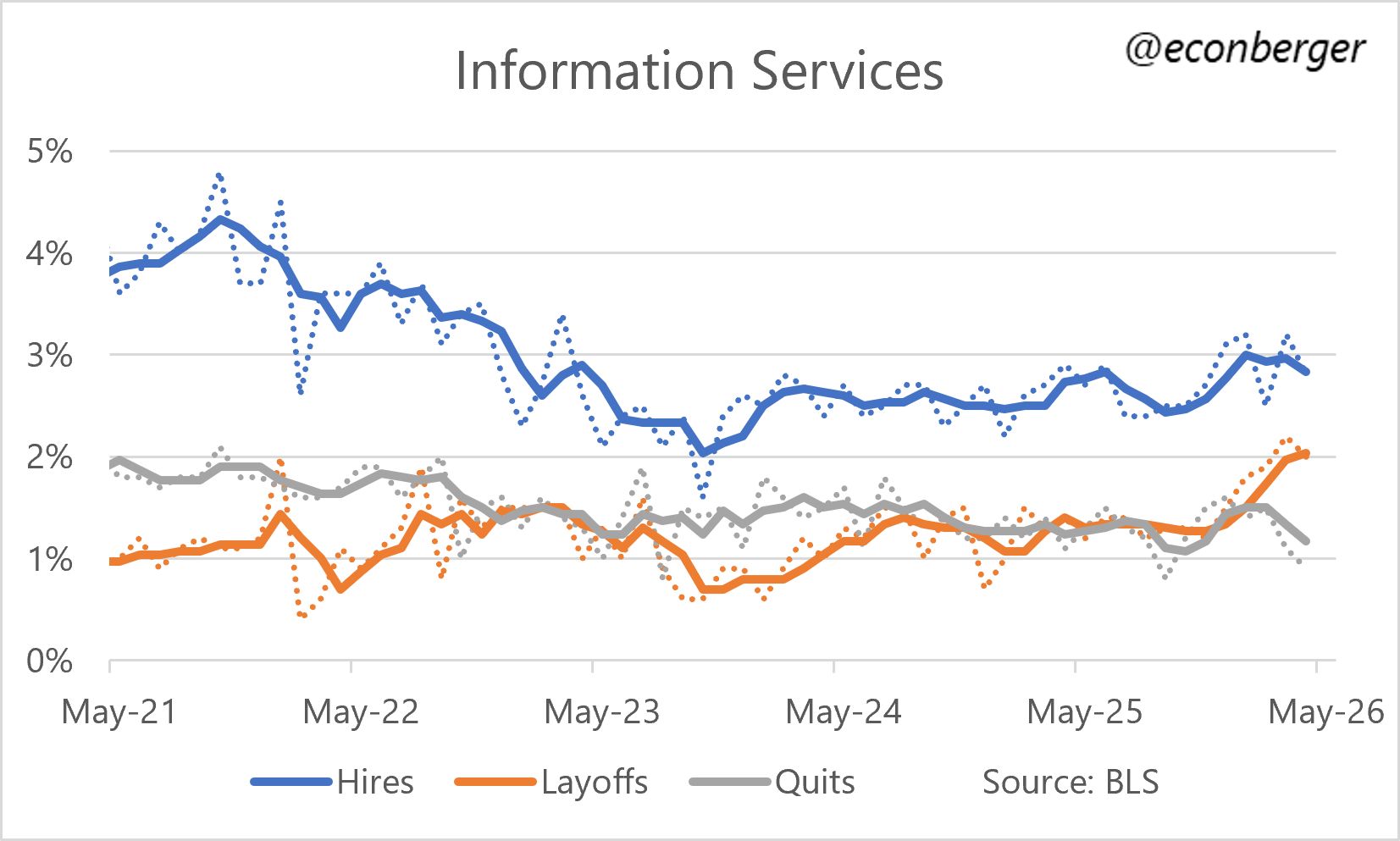

Finally, I’ll wrap by looking at the information services sector, which has a messy and imperfect overlap with the tech sector and is undergoing real disruption: hiring and layoffs are both elevated relative to last year. This sector is small but my “layoffs are very low” statement probably seems really alien there.

I’m not saying a hiring boom is impossible. (Though it is unlikely.) But the openings data we’ve seen recently definitely doesn’t imply one is imminent.

Typo: "You really do have to squint: the hiring rate has averaged 3.32% in the first 5 months of 2026, vs. 3.27% in the final 6 months of 2026." >> should be final 6 months of 2025.

The most interesting line in this piece is buried in the middle: the hiring thaw may be driven by equity prices encouraging businesses to hire and consumers to spend. That is a reflexivity loop worth naming. Equities are near-unanimously overweight in the institutional consensus.

If the labour market's marginal improvement depends on equity prices holding, then the Fed's next move and the equity market's next move are not independent variables. They are the same variable described twice.