2025 Labor Market Outlook

The Pendulum Swings Back

TL;DR: The most likely labor market outcome for 2024 is an end to the labor market cooling process we’ve experienced over the past 2.5 years.

This piece is structured as:

Prologue

The Big Picture

The Base Case

Upside Risks

Downside Risks

More below chart.

1. Prologue

I have mixed feelings about year-ahead outlook pieces because they are almost universally wrong from a forecasting perspective, and if they happen to be right about something, it’s usually by accident.

That said, I wrote this hoping to outline what I think are the “known knowns” and “known unknowns” about the labor market in the coming year. More than a typical year, in which this kind of outlook depends on the answers to a few well-understood questions, this year’s uncertainty involves big proposed policy changes whose adoption, magnitude, timing and impact is TBD.

Nevertheless, I hope this essay is useful and informative from a scenario planning perspective, even if there are tons of “ifs”, “maybes” and “probablys”. Feedback is always welcome and thanks for reading!

2. The Big Picture

In my 2024 labor market outlook, I predicted “Soft Landing, But Lots of Taxiing on the Runway”. I was wrong in two respects. First, inflation made less progress than I anticipated. Second, I anticipated that the labor market would stop cooling. Neither of those things happened!

Inflation did moderate a little bit in the first half of the year, but it’s not clear progress is ongoing - it’s even possible we’re experiencing some regress.

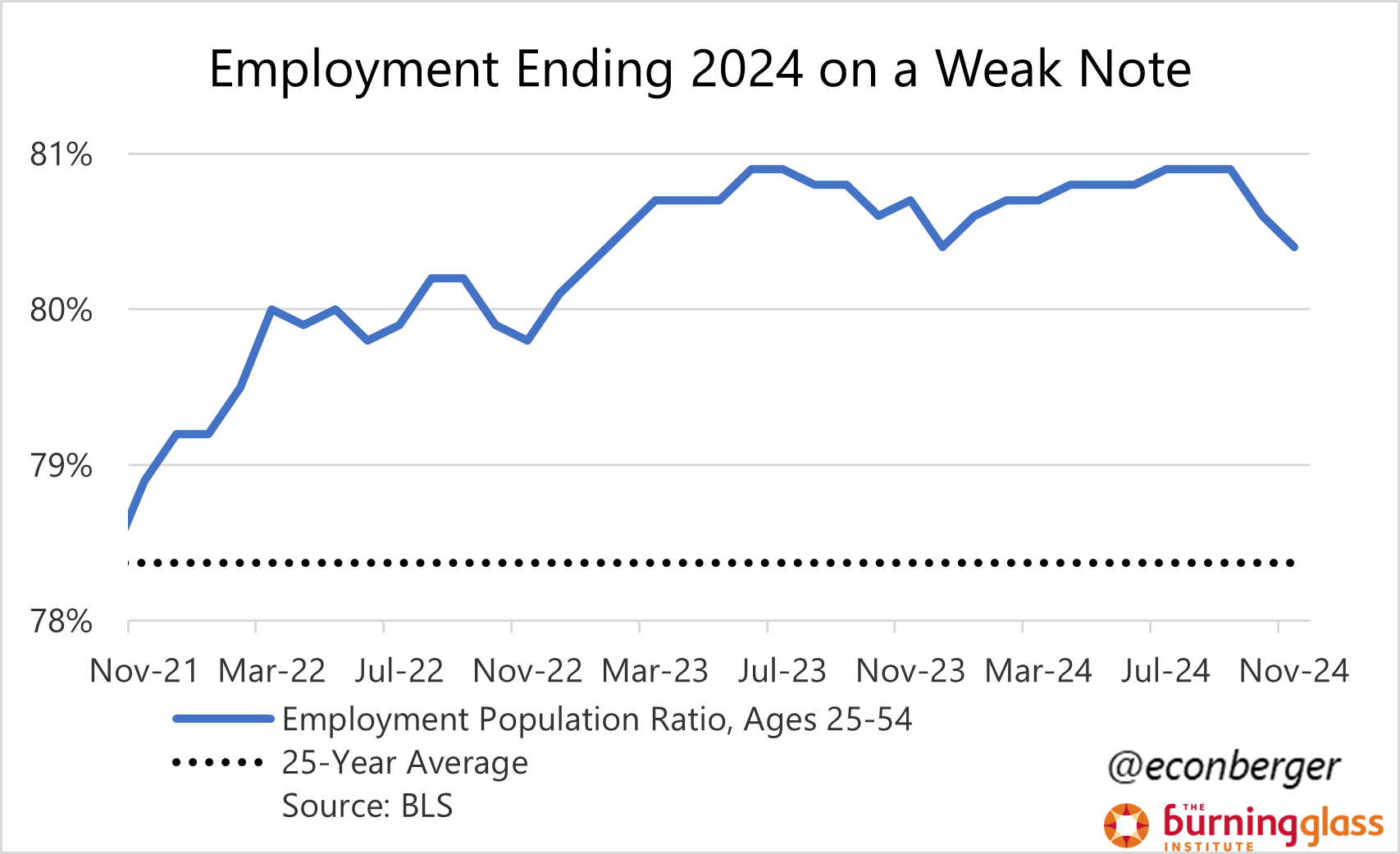

And on the labor market side, a wide range of labor market indicators - the unemployment rate, the prime working age employment population ratio, the share of folks working part time for economic reasons, hiring and quits rates, the list goes on - are at least modestly weaker than they were a year ago.

I was wrong in 2024, but there’s always next year, and I think in 2025 the labor market cooling will actually pause. US firms are already more optimistic about future headcount plans than they were a year ago. The factors pushing in this direction have intensified. I’ll go through those factors in the base case section below.

3. The Base Case

A. The Fed’s Balancing Act

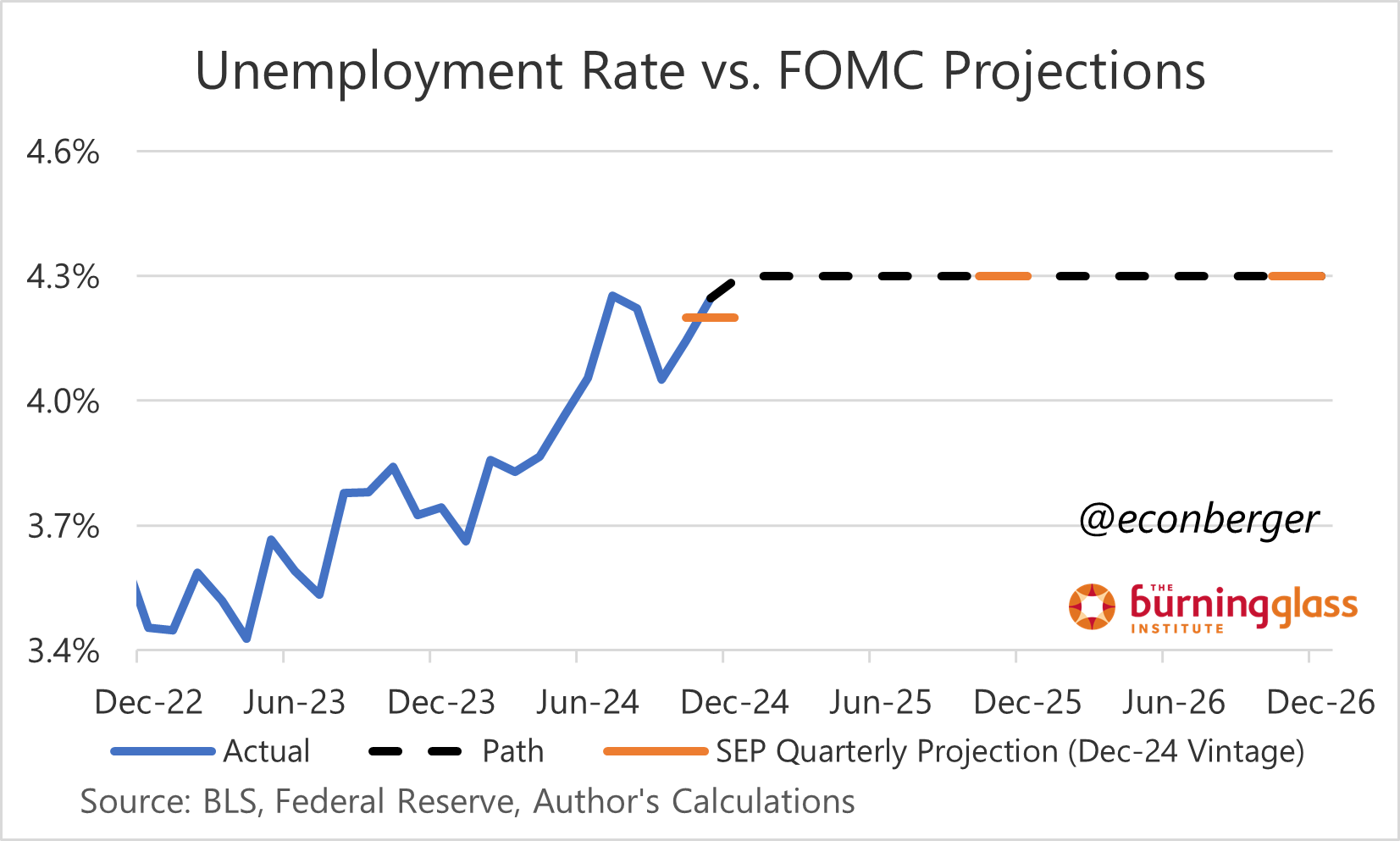

In press conferences this year, Chair Powell has repeatedly indicated that a core aim is preserving what he and the Federal Reserve consider to be a good labor market; the Fed’s December projections (conditioned on “appropriate monetary policy”) have the unemployment rate rising modestly further from current levels, to 4.3%, and staying there. The messy inflation data of the past few months has complicated the Fed’s plan, but barring a meaningful resurgence in price growth (currently running around 2.5%-3.0% annualized, depending on your preferred metric), this goal is likely to remain in place.

However, unless we see a rapid, sustained and dramatic improvement in inflation from where we currently are, there are limits to how far the Fed’s labor market support will go - they’ll want stabilization, not renewed labor market overheating. To the degree that the other factors below push in that overheating direction, I’d expect them to be offset with less Fed easing (and, in extremis, tightening).

B. New Administration Policy: Immigration

2024’s data mix was enigmatic: the aforementioned labor market cooling, coupled with strong growth in employment (at least in the first half of the year) and GDP. Two factors square that circle: (possibly temporary, possibly durable) acceleration in productivity, and a sharp increase in immigration. Labor supply growth has outrun labor demand growth, leading to an increase in labor market slack.

Immigration is already slowing, as southwest border encounters have fallen sharply. And there’s room for it to decrease further. Visa issuance is still more elevated than it was before the pandemic (though not all immigrant recipients are eligible to work); I’m guessing the executive branch has some ability to slow this flow. And something even more extreme is being mooted: mass deportations, which would lead to not just lower population growth but possibly a contraction of the working population.

My best guess is that the crackdown on immigration will be only partial. Nevertheless, even partial implementation is probably going to result in the mirror image of the early 2024 data: weaker employment (and GDP) growth and a reheating labor market. It’s also the kind of policy that will result in less Fed easing.

C. New Administration Policy: Tax Cuts

One of the biggest legislative milestones of the first Trump presidency was a big tax cut, and the second Trump presidency is likely to go for a repeat. It’s not going to be as easy this time; the GOP has a much narrower majority in the House. That said, I’m assuming a large tax cut is probably coming and that only part of it, if at all, will be offset by higher tariffs and lower spending.

To the degree that this deficit-expanding tax cut is implemented, my expectation is that it will expand demand. Like the expected crackdown on immigration in section B, it will induce tighter labor markets and lower unemployment. It would probably also lead to less Fed easing. But unlike immigration policies, it’s also likely to boost employment (and GDP growth), at least in the short run, like any demand-side policy.

D. Other New Administration Policies: Tariffs, Spending Cuts

Two other big policy ideas being thrown around are tariffs and spending cuts. On the tariff side, I’d imagine that any impact would be primarily reallocative: over time, people and resources shift away from sectors that aren’t covered by tariffs, and toward ones that are. There may also be a negative impact on demand, as with any tax, and that could hurt employment. (Though of course, if coupled with big cuts in other taxes…)

On the spending cut side, I’m not sure how probable big, substantive cuts (vs flashy but cosmetic ones) are - it’s hard to get big legislation through Congress with a narrow majority and spending cuts generate a lot of veto points. But if they do happen, they’ll be contractionary. How much will this hurt employment? Depends on how hot the labor market is. Perhaps in a worker shortage environment triggered by tax cuts and immigration restrictions, the job losses by spending cuts (especially if spread over time) will be relatively ephemeral. And just like big unfunded tax cuts and immigration crackdowns could lead the Fed to tighten the monetary belt, spending cuts would be accommodated by Fed loosening.

4. Upside Risks

In the prior section I outlined reasons why we’d expect the labor market to stabilize. but it’s quite conceivable that those forces overshoot (especially the ones generated by political actors), leading to renewed labor shortages and a full-blown reheating of the labor market: the demand side being goosed by tax cuts, the supply side being constricted by immigration blockage. In the short run that would lead to falling unemployment, rising hiring and quits, and reacceleration in nominal wage growth.

If this happens the medium run the Fed would respond with tighter monetary policy than in the baseline - possibly putting renewed labor market cooling back on the docket for late 2025, or 2026.

5. Downside Risks

It’s harder for me to conjure pessimism about 2025’s labor market outcomes, even if we have some additional cooling ahead of us before all those stabilization (and possibly reheating) mechanisms fully kick in.

But if I really strain my imagination, I can come up with some. I assign low probability to all of them:

Maybe there are underlying dynamics in the labor market that will frontload sharp further deterioration before sufficient Fed easing or labor-shortage-inducing policies by the new administration kick in. This is the “small, gradual increases in the unemployment rate often turn into big, rapid ones” argument. I don’t see any signs of this dynamic right now, but you never know.

A second possibility is that we get a turbocharged version of what’s described in the upside risks section - severe labor shortages return with a vengeance, with clear leakage into consumer price inflation (not just wage growth). In that case, you could imagine the Fed slamming the breaks, suddenly pushing the economy into reverse. But it’s hard to imagine this happening quickly enough to put the 2025 labor market at risk.

A combination of higher tariffs, sharp cutbacks in government spending without large cuts in other taxes or easing in monetary policy leads to lower aggregate demand and weaker labor markets. This seems like a fanciful scenario!

Maybe some of the frothiness in financial markets leads to a popped bubble and sudden tightening in financial conditions, with fiscal and monetary policy underreacting until it’s too late.

If we’re unlucky enough to experience one of these, feel free to say I told you so relentlessly! It’ll be on my mea culpa recap for the 2026 labor market outlook.

Would you be willing to expand upon the thought that a repeat/expansion of tax cuts will increase demand? It would seem that if this round of cuts mirror the TCJA that the vast majority of savings will go to corporations/the ultra-wealthy which, I would expect, would result in asset inflation (equities, etc.) rather than general inflation since an additional dollar sent to the ultra-wealthy results in much lower velocity than the same dollar sent to those earning sub-$100k/yr. Reviews of the TCJA generally found that it had minimal, if any, effect on economic growth.