JOLTS Recap (August)

The "Great Stay" Becomes Stay-ier

TL;DR: This is a really tough market for job seekers, with hires at early 2010s levels. Quits fell to their lowest level since 2015.

In this recap I talk about:

The Big Picture

Careful with Job Openings

1. The Big Picture

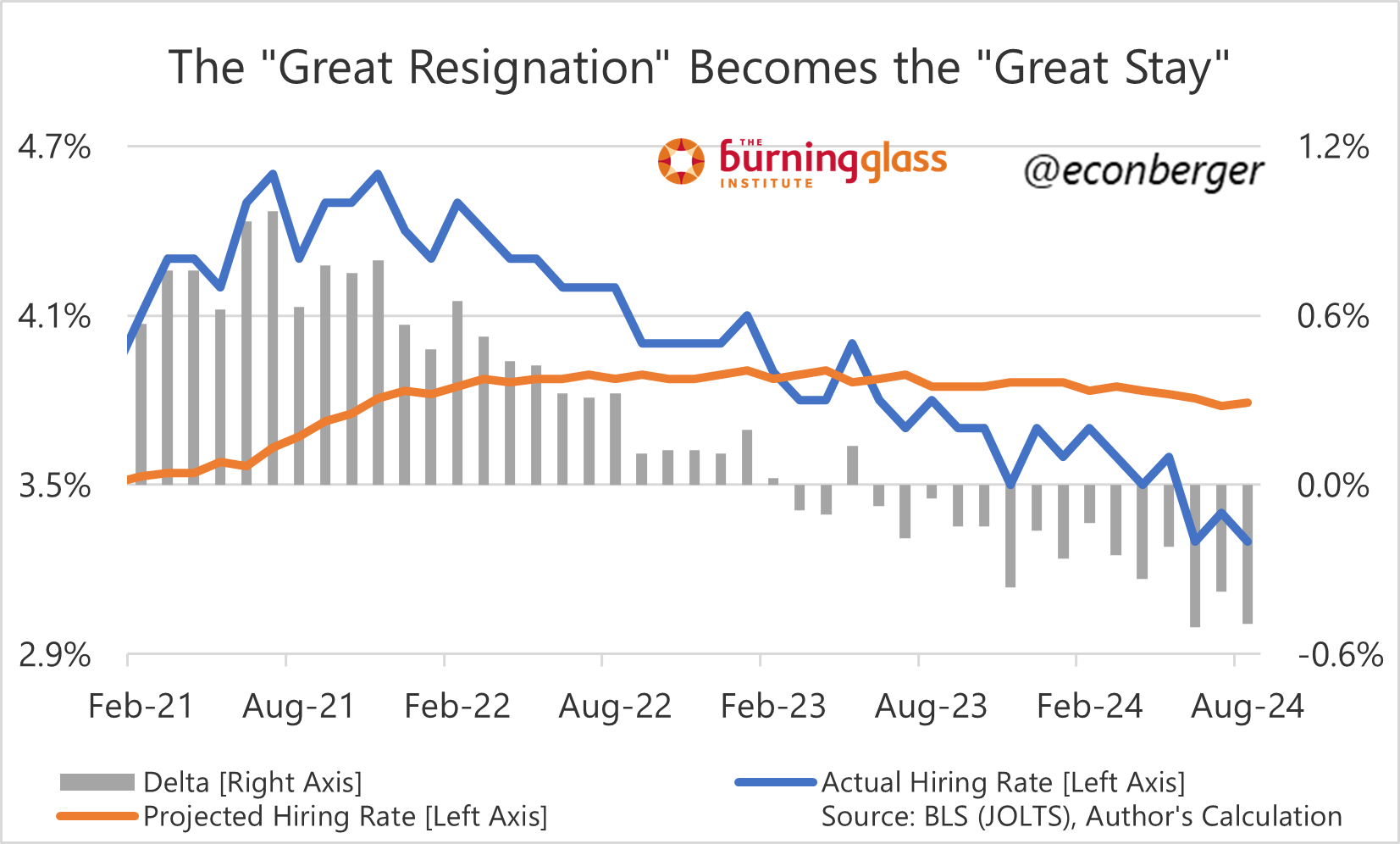

This is a really tough job market for job seekers. The hiring rate fell to 3.3% in August, matching its lowest level since 2013 (excluding the brief COVID period). In the 2010s expansion, we would have typically expected this level of hiring with an unemployment rate just over 8%!

The good news is that monetary policy will eventually stabilize hiring. The bad news is that it’s not going to happen immediately (with luck, in early 2025), and even after stabilization happens, upside will be limited. The Fed doesn’t want to reheat the labor market, it just wants to avoid further cooling. Looking for a job could remain un-fun for quite a while.

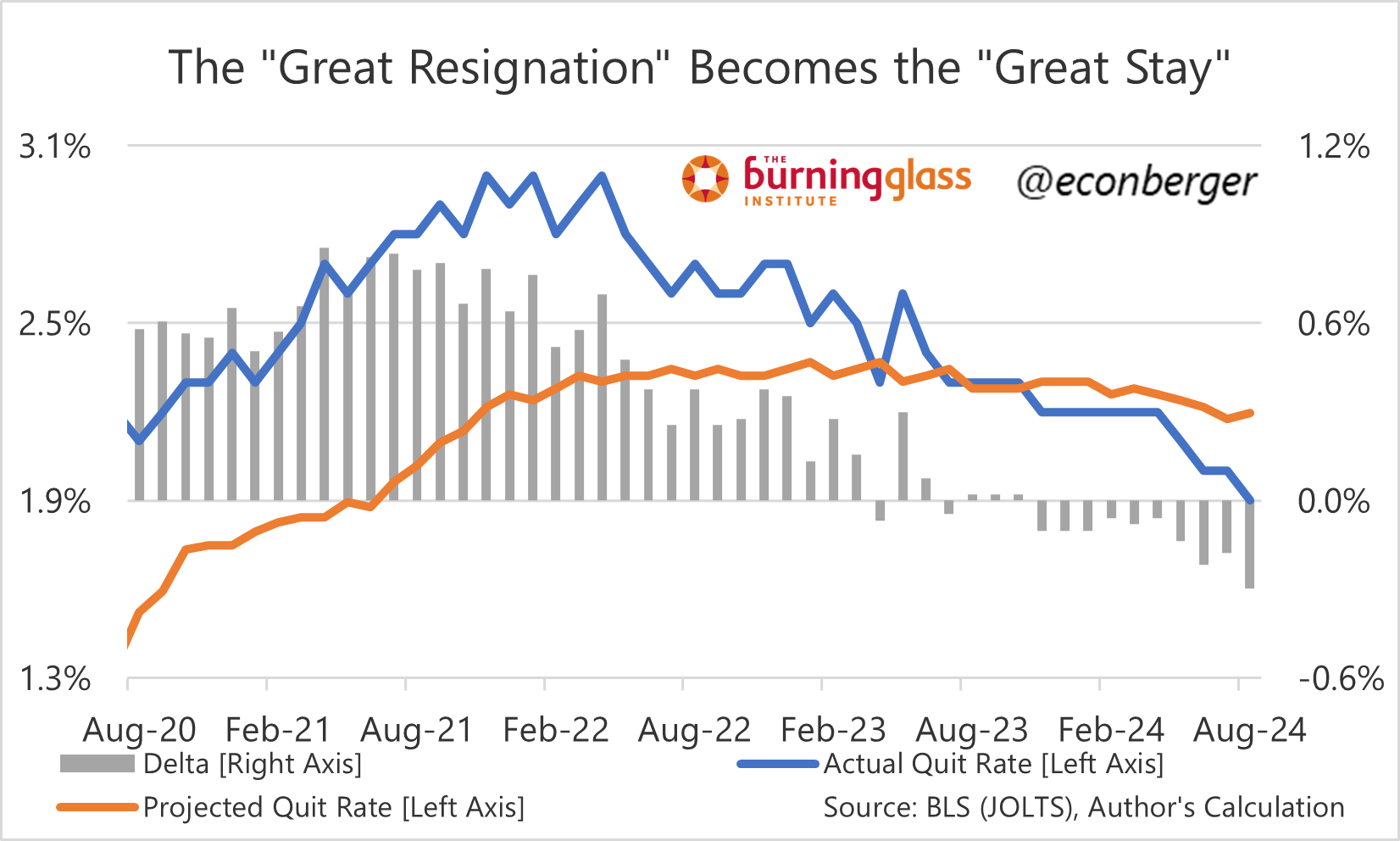

Folks know job seeking opportunities are slim, and as a result they’re holding tight to their jobs. The quit rate fell to 1.9%, its lowest level since 2015 (excluding the brief COVID period). In the 2010s expansion, we would have typically expected this level of quits with an unemployment rate of 5.5%-6.0%.

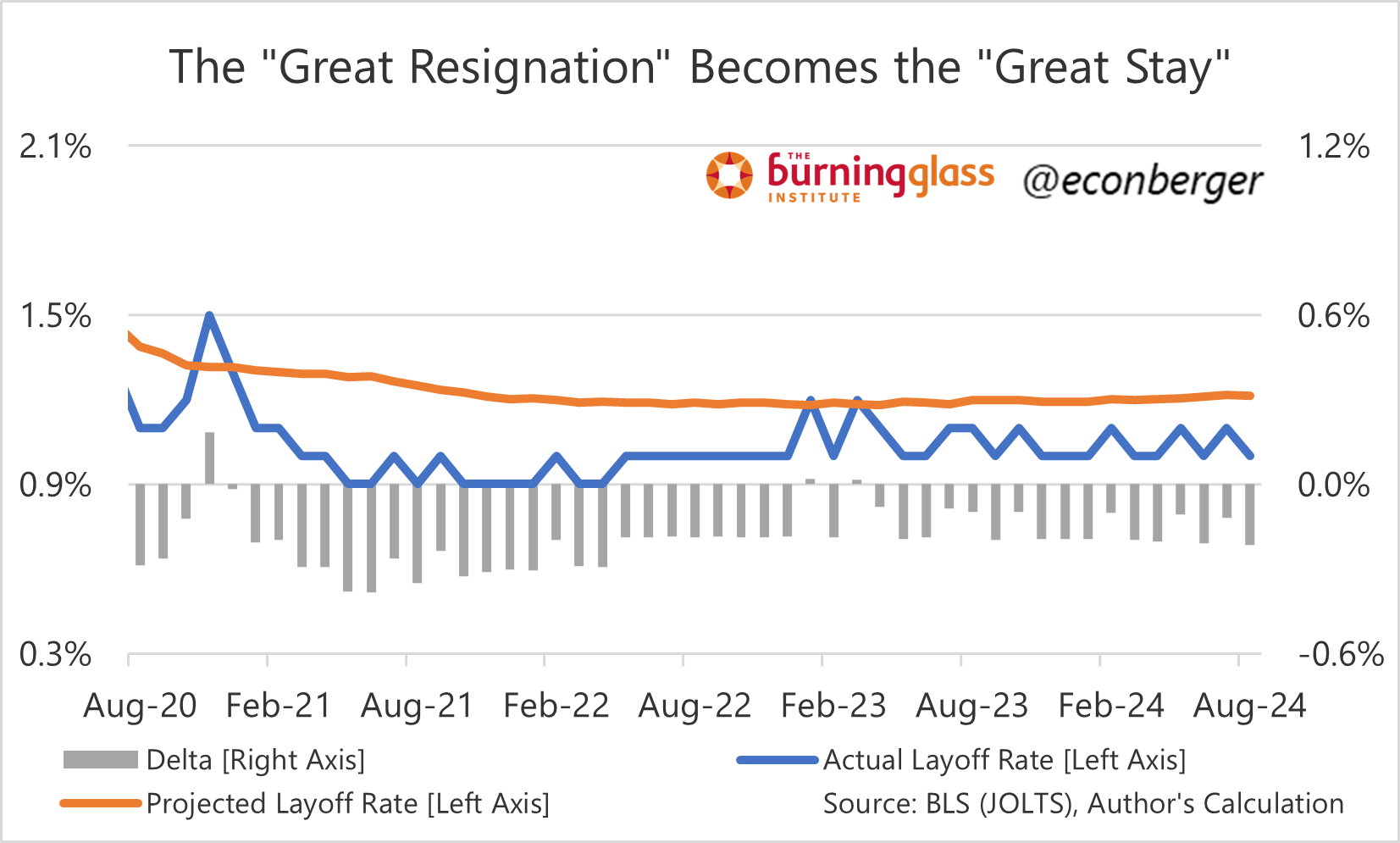

The one silver lining is that layoffs remain extremely low. If you have a job, you’re relatively secure in it. It’s still an open question at what point employers shift their headcount management strategy from “fewer hires” to “more layoffs”.

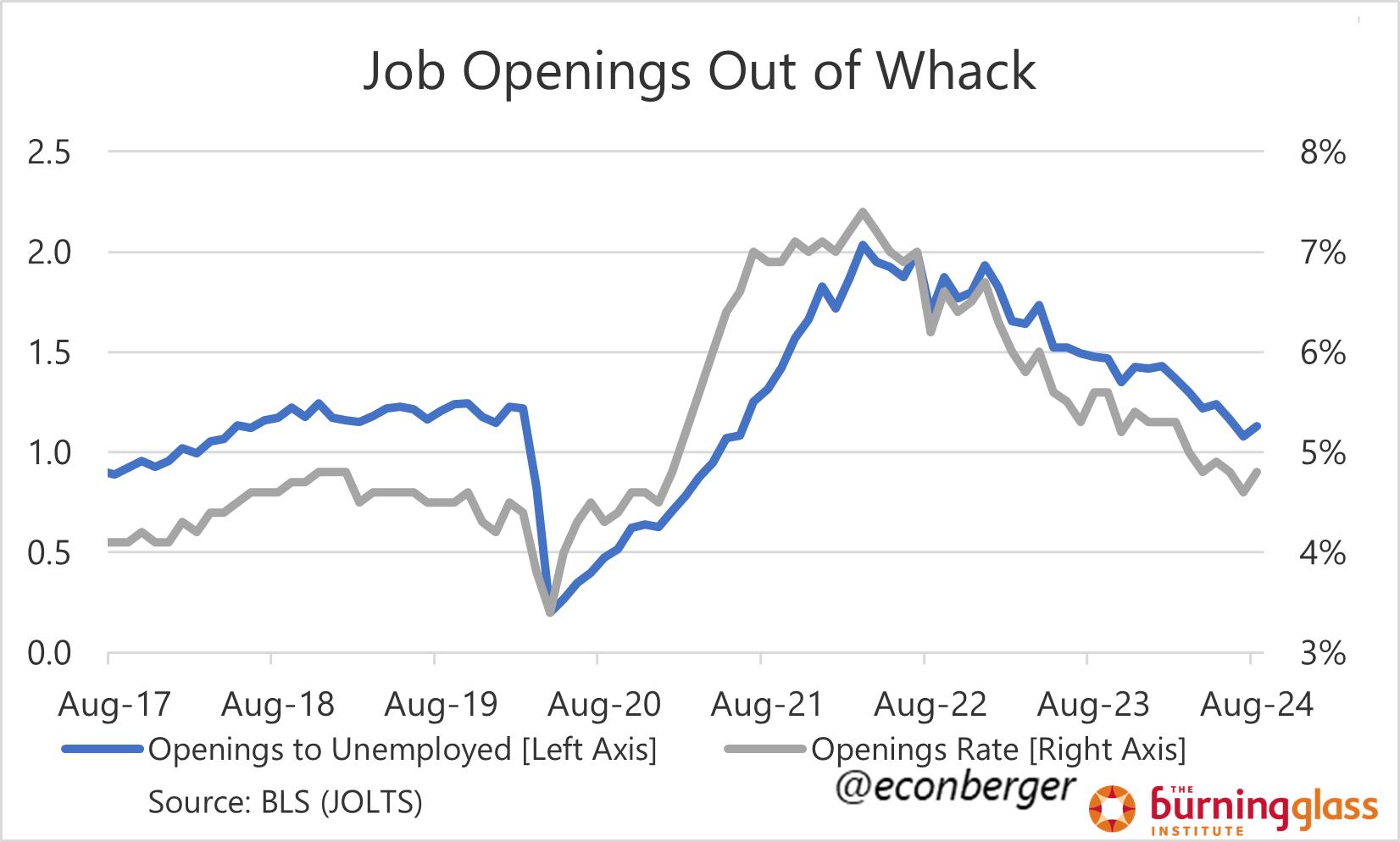

2. Careful with Job Openings!

I’m a big fun of Fed Chair Jay Powell - an avid data consumer after my own heart. In a speech yesterday, he rattled off his perspective about the labor market, which contained one big red flag for me - the Fed’s ongoing fandom of job openings data.

It’s a strongly held belief of mine that job openings are the least valuable portion of the JOLTS report. For whatever reason, the cyclically-adjusted trend in job openings is positive. Therefore, a “high” ratio of openings to unemployed will tend to overstate how hot the job market is relative to past cycles.

And that means that an openings/unemployment ratio of 1.13 (about where it was in mid-2018) and an openings rate of 4.8% (late 2018) overstate the strength of the labor market significantly. Employers may say they have a lot of openings, but as economists we believe in revealed preference: their hiring behavior looks quite different. If you’re using job openings to conclude that the job market is strong, you are IMHO making a mistake.