A Labor Market Economist's Take on Wednesday's Fed Decision

A Labor Market Economist's Take on Wednesday's Fed Decision

A little late, but very welcome

TL;DR: The Fed’s decision to lower its policy rate by 50 basis points (with more on the way) is welcome news for stabilizing the cooling labor market. However, labor markets are likely going to cool by a little more than the Fed currently expects.

I’m a labor market guy, not a Federal Reserve expert, so this brief post will focus on the Fed’s decision entirely from that lens.

A brief table of contents:

What Happened (& Will Happen)

The Fed Statement

The Economic Projections

Chair Powell’s Press Conference

1. What Happened (& Will Happen)

The Federal Reserve lowered its policy rate for the first time since 2020, by 50 basis points. Moreover, this is probably not the final cut. The Fed’s economic projections (more on this later) indicate that, if the economy evolves as they expect they will reduce interest rates by another 50 basis points by year-end, and another 100 basis points after that.

It’s worth emphasizing these forecasts are of “appropriate monetary policy” given the economy evolving as the Fed expects. Think of it as a conditional prediction: “if the economy does this, we will do that.” The Fed’s economic projections are often wrong, as are all economic forecasts. So the Fed might ease policy more than currently expected (if inflation comes down more than expected, or the labor market worsens more than expected), or by less than expected (if inflation remains stubbornly high or the labor market regains its vigor).

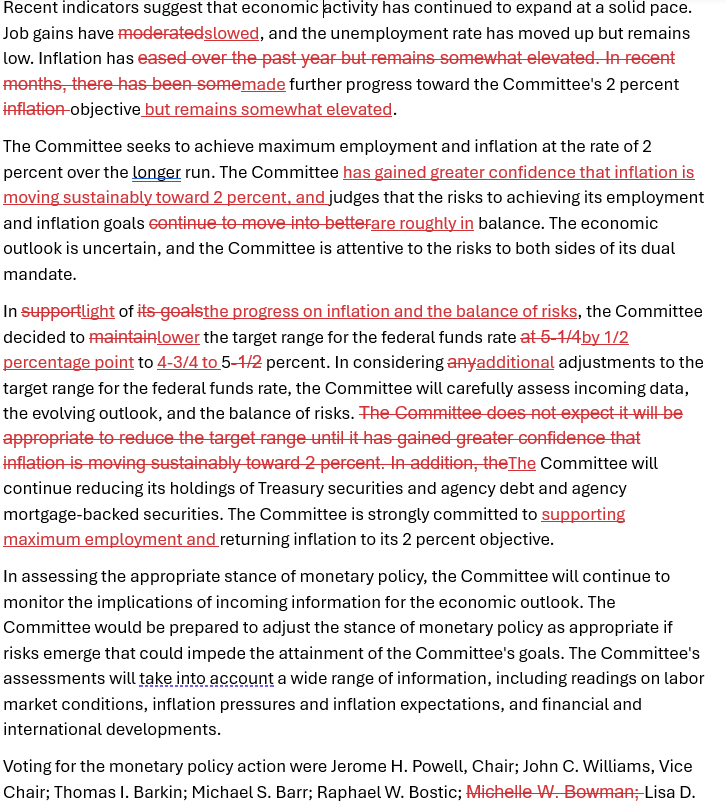

2. The Fed’s Statement

Microsoft word has a convenient feature to compare two versions of the same document; below is a screenshot of its comparison between the July 31st and September 18th FOMC1 statements.

There are lots of interesting things here, but three stand out to me:

The 1st paragraph shift in characterization of job gains from “moderated” to “slowed”.

3rd paragraph introduction of “supporting maximum employment”.

No change to the 1st characterization “the unemployment rate… remains low”.

On 1 & 2, labor market worries are weighing on the Fed (appropriately so - more on this later) in a way that’s different from 6 weeks ago. Not surprisingly, they’re committing to putting a floor under the labor market as long as inflation continues to play ball.

On 3, calling 4.2% unemployment “low” is fine, but I wonder if it will still apply in the (IMHO probable) event that unemployment ends up in the 4.5%-5.0% range. And it will certainly have to change if we’re unlucky and unemployment heads north of 5%. Hopefully a statement with “the unemployment rate is elevated” is not in our future.

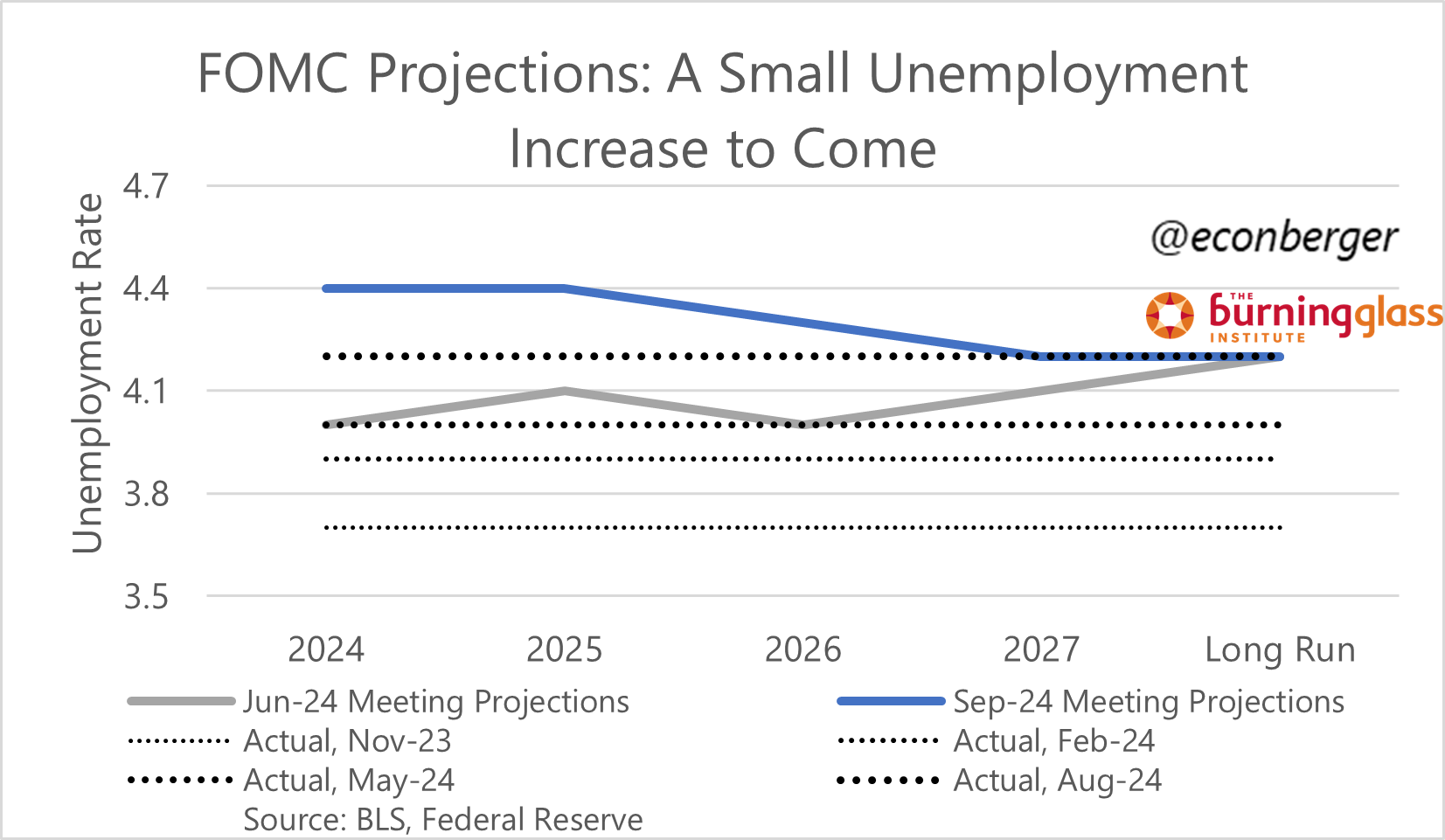

3. The Economic Projections

The Fed 2024-25 projections for the unemployment rate increased relative to the prior iteration, in June. While the increase’s magnitude was small, the unemployment rate path had a notable change in shape too.

Three months ago the Fed anticipated that, over an undetermined time span, the unemployment would gradually drift up from 4.0% to 4.2%. Now, with the unemployment rate already at 4.2% a few years ahead of schedule, they anticipate a slight further increase to 4.4% before gradual drift back down to 4.2% starting in 2026.

First off, this gives us a useful benchmark for what would cause the Fed to ease policy faster and/or by more than they currently expect - the unemployment rate breaching that 4.4% forecast in the near term.

Second, I think this forecast is a little too optimistic. We’re likely headed to the 4.5%-5.0% range, even without a recession. The dynamics that are pushing unemployment up will probably be in place a little while longer before Fed action convinces employers to stop cutting back on hiring.

The Fed’s commitment to preserving maximum employment (assuming no big inflation curveballs) means that I expect the unemployment overshoot will be small. It’ll take a recession to cause a large overshoot.

I think a creative interpolation of these projections - the unemployment rate breaches 4.4% in early 2025, then returns back to 4.4% by late 2025 - allows us to square that circle. But just keep this in mind as the data evolves in the next 6 months.

4. Chair Powell’s Press Conference

Fed Chair Powell’s press conference is always a treat for data nerds. You get to see the nation’s smartest business reporters asking Powell well-informed and sometimes esoteric questions about the economic outlook and its implications for monetary policy.

A few things that stood out:

In response to Jo Ling Kent (CBS News)’s question about what message he would give the American people, Powell said: “I would just say that the U.S. economy is in a good place, and our decision today is designed to keep it there.”

People suggested pre-meeting that a 50 basis point cut could come off as “panicked”. Powell sounded extremely unpanicked - if anything, he should be a little more worried than he sounded.

In response to Rachel Siegel (Washington Post)’s question about which data he is closely following, he mentioned (1) unemployment (2) participation (3) wage growth ("a bit above" where the Fed wants it to be +"coming down") (4) vacancies/unemployed [NO JAY NO!!!] and (5) quits. “This is still a solid labor market... downside risks to employment have increased."

Jeanna Smialek (NY Times), Colby Smith (Financial Times) and Victoria Guida (Politico) challenged Powell on his confidence that the unemployment rate will top out around 4.4%. I didn’t find Powell’s answers here to be fully satisfactory!

Neil Irwin (Axios) and Simon Rabinovitch (The Economist) asked Powell about how he processes the nonfarm payrolls data, given recent large revisions. And Powell suggested he shades down the recent numbers in anticipation of possible future downward revisions.

For folks who aren’t Fed fanatics: the Federal Open Market Committee (FOMC) is the body that decides on interest rates. It’s a subset of the most senior Fed officials. I’m going to use “Federal Reserve” and “FOMC” interchangeably in this post, which is unforgivably sloppy.